You pay your credit card bill in full every month. You never carry a balance. Your credit score should be perfect, right? Yet somehow, your score seems stuck, or worse, it drops unexpectedly after months of responsible use. The culprit may not be how much you spend, but when you pay.

Most consumers assume that as long as they pay by the due date, their credit report will reflect their responsible behavior. This assumption is wrong, and it costs millions of Americans valuable credit score points every month. Understanding the difference between your payment due date and your statement closing date unlocks one of the simplest and most powerful strategies for optimizing your credit utilization.

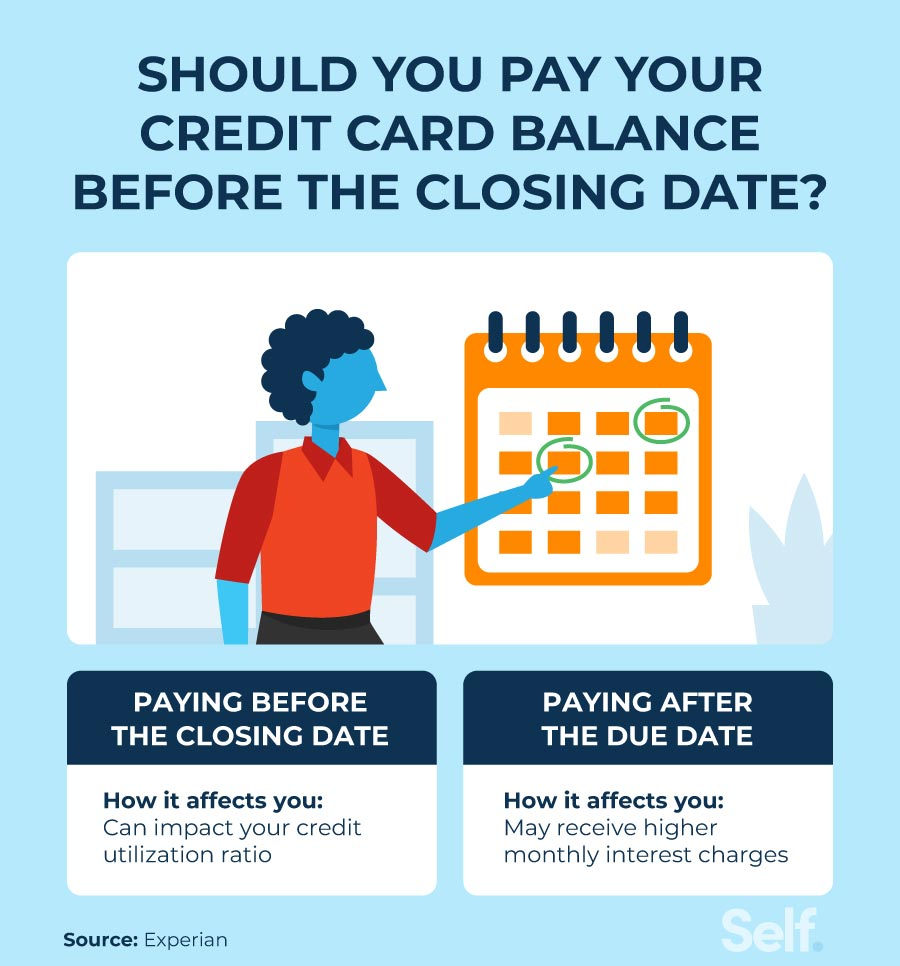

The Critical Difference: Closing Date vs. Due Date

Your credit card has two important dates each month, and confusing them is the root of the problem.

The statement closing date is the day your credit card issuer prepares your monthly statement. On this date, they take a snapshot of your account balance and report it to the credit bureaus. This reported balance becomes the “credit utilization” that appears on your credit report and affects your score.

The payment due date comes later, typically 21 to 25 days after your statement closes. This is the deadline by which you must pay at least the minimum to avoid late fees and penalties. When you pay by this date, you avoid interest and keep your account in good standing, but the balance reported to the bureaus has already been captured.

The crucial insight is that paying on the due date does nothing to lower the balance that was already reported on the closing date. If you spent heavily during the month, that high balance is already on your credit report, potentially damaging your score for the next month.

How the “Due Date Trick” Actually Works

The strategy is simple once you understand the timing. Instead of waiting until your payment due date, you make a payment a few days before your statement closing date. By paying down your balance before the snapshot is taken, you ensure that a low balance is what gets reported to the credit bureaus.

Here is a step-by-step breakdown:

Step 1: Find your statement closing date. Log into your online account or check your most recent statement. Look for the date labeled “statement closing date,” “cycle date,” or “period end date.” This is the date your issuer summarizes your activity for the month.

Step 2: Pay your balance down before that date. A few days before your statement closes, log in and make a payment bringing your balance to your target level. For optimal scoring, aim to have between $0 and 10% of your credit limit reported. If you want to follow the AZEO method, leave a small balance on one card and bring all others to zero.

Step 3: Let the low balance report. When your statement closes with this low balance, that is what gets sent to the credit bureaus. Your utilization looks excellent, and your score benefits.

Step 4: Pay the remaining balance by the due date. After the statement closes, you will still have a balance showing on that statement. Pay this amount in full by the actual payment due date to avoid interest and late fees.

Why This Works: The Memoryless Nature of Utilization

This strategy works because of a fundamental feature of most credit scoring models: utilization has no memory. Current FICO and VantageScore models only care about the most recently reported utilization from each account. A high balance one month is forgotten as soon as a low balance is reported the next month.

This means you can spend freely throughout the month, make a strategic pre-closing payment, and present a perfect utilization snapshot to the bureaus without changing your actual spending habits. You get the benefit of using your credit card for rewards and convenience while still optimizing your score.

The exception is newer models like FICO 10T and VantageScore 4.0, which incorporate trended data and look at your utilization patterns over the past 24 months. These models, increasingly used by mortgage lenders, reward consistent low utilization rather than just last-minute optimization. For these models, the due date trick still helps, but maintaining low balances month after month matters even more.

Real-World Examples

Consider Sarah, who has a single credit card with a $1,000 limit. Throughout the month, she charges about $800 in normal expenses: groceries, gas, dining out. She pays the full $800 on her due date, thinking she is being responsible.

On her statement closing date, before she paid, her balance was $800. That $800 was reported to the credit bureaus, showing 80% utilization. Her credit score drops 30 to 50 points despite her perfect payment history.

Now consider Sarah using the due date trick. A few days before her statement closes, she logs in and pays $750 of her $800 balance. When the statement closes, only $50 is reported, showing 5% utilization. Her score stays high. After the statement closes, she pays that remaining $50 by the due date and owes nothing in interest.

Same spending, same responsible habits, completely different credit score impact.

How Much Can This Improve Your Score?

The potential improvement depends entirely on your starting utilization. If you were previously letting high balances report, the gain can be dramatic.

A drop from 80% utilization to 10% utilization can boost your score by 30 to 60 points or more in a single month. For someone hovering near the 30% threshold, moving down to 10% might yield 10 to 20 points. Even moving from 10% down to 3% can squeeze out a few additional points for those pursuing top-tier scores.

The greatest benefits go to those with the lowest credit limits. A $500 limit card can hit 50% utilization with a single $250 grocery run. For these consumers, the due date trick is not just optimization; it is essential for maintaining decent credit while using their cards at all.

Common Questions and Pitfalls

Will this strategy cost me interest? No, as long as you pay the remaining statement balance by the actual due date. You are simply prepaying part of your balance before the statement generates, not carrying debt.

Does this work for all credit cards? Yes, for all standard revolving credit cards. Store cards, secured cards, and rewards cards all follow the same statement closing date reporting pattern. Charge cards like American Express Gold or Platinum work differently and may not report utilization the same way.

What if I have multiple cards? The same principle applies to each card individually. Pay down each card before its respective statement closing date. If you are using the AZEO method, you will leave a small balance on one strategically chosen card.

Do I need to do this every month? Only if you care about your score every month. For everyday credit health, simply paying on time is sufficient. Use the due date trick in the one to two billing cycles before applying for a major loan like a mortgage or auto loan.

Will my credit card company penalize me? No. Credit card companies do not care how often you make payments. Some may view frequent payments as slightly unusual, but it does not harm your account or relationship with the issuer.

The Bottom Line

The due date trick is not about spending less; it is about timing your payments to match how credit scoring actually works. By understanding that your statement closing date determines what gets reported, you transform from a passive consumer into an active manager of your credit profile.

Find your statement closing dates. Mark them on your calendar. Make a habit of checking your balances a few days beforehand and paying down to your target level. Let that low balance report, then pay the rest by the due date.

This simple shift in timing costs nothing, requires minimal effort, and can add significant points to your credit score exactly when you need them most. In the game of credit optimization, knowing when to pay is just as important as knowing how much to pay.

Leave a Reply