You see it on credit card offers, loan advertisements, and mortgage paperwork: the term APR, always presented as a percentage. Lenders are required by law to show it to you, and financial experts tell you to pay attention to it. But if you have ever found yourself wondering what APR actually means and why it matters for your wallet, you are not alone. Understanding this number is one of the most important skills you can develop for making smart borrowing decisions.

APR stands for annual percentage rate, and it represents the true cost of borrowing money over the course of a full year . Unlike a simple interest rate that only tells you the cost of the principal amount you borrow, APR wraps in many of the fees and charges associated with getting a loan . This makes it the most accurate tool for comparing different loan offers side by side.

The Simple Definition of APR

At its core, APR is the annual cost of a loan expressed as a percentage . Think of it as the price tag on borrowed money. When you see a loan advertised with a 9.99 percent APR, that means you will pay roughly 9.99 percent of the loan amount in interest and fees each year, spread across your monthly payments.

The federal Truth in Lending Act requires lenders to disclose the APR on consumer loan agreements . This law exists because without a standardized measure, lenders could hide the true cost of borrowing behind confusing terms and buried fees. The APR requirement forces transparency, giving you a fighting chance to understand what a loan will actually cost you.

APR Versus Interest Rate: Understanding the Critical Difference

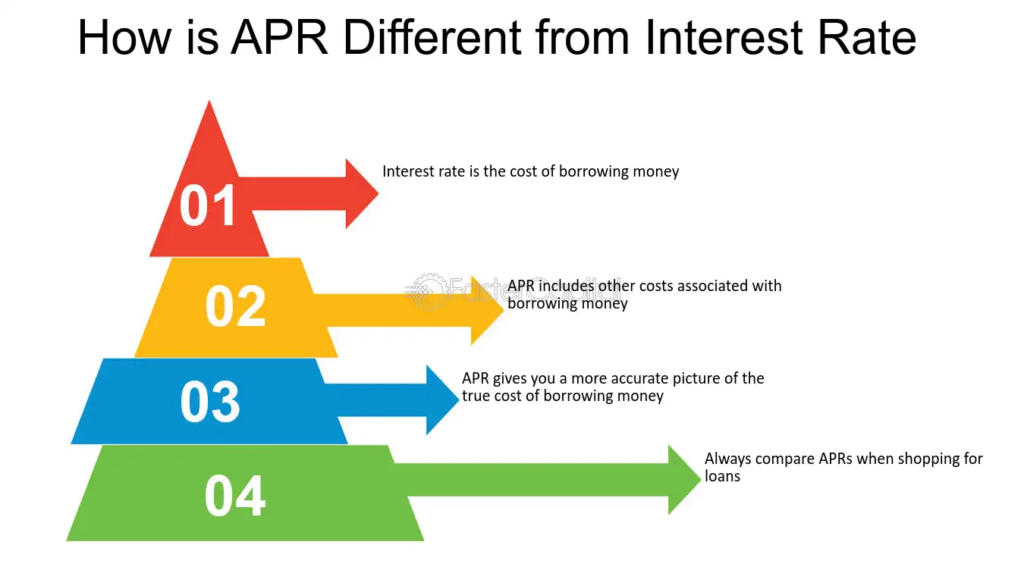

Many borrowers use the terms APR and interest rate interchangeably, but they are not the same thing. The difference between them is where the true cost of borrowing often hides.

Your interest rate is simply the cost you pay to borrow the principal amount of your loan . It is expressed as a percentage and represents the annual cost of the money you receive. If you borrow twenty thousand dollars at a five percent interest rate, you will pay about one thousand dollars in interest during the first year, assuming you make only minimum payments.

APR, however, takes a bigger view. It includes your interest rate plus any additional fees and charges required to get the loan . These can include origination fees, discount points, mortgage insurance, underwriting fees, document preparation fees, and certain closing costs . By rolling these expenses into a single percentage, APR shows you the all-in cost of borrowing.

For example, imagine you are comparing two loans for the same amount. One has a 6.5 percent interest rate with three thousand dollars in fees. Another has a 7 percent interest rate with no fees at all. Looking only at interest rates, the first loan appears cheaper. But when you calculate the APR, the second loan might actually cost you less over time because you are not paying thousands of dollars upfront . This is why APR exists: to help you make apples-to-apples comparisons.

What Fees Are Included in APR?

Understanding what goes into APR helps you evaluate whether you are getting a fair deal. While different types of loans may include slightly different fees, the general categories remain consistent across most borrowing situations.

For mortgages, APR typically includes the interest rate, loan origination fees, discount points you choose to pay, private mortgage insurance if your down payment is below twenty percent, underwriting fees, and certain administrative costs . These are expenses you must pay to get the loan, so they belong in the true cost calculation.

For personal loans and credit cards, APR generally includes the interest rate plus any origination fees charged by the lender . Some loans, like those offered by Discover, charge no fees at all, which means the interest rate and APR are identical . This is worth looking for when shopping around.

Not every expense appears in your APR. Fees for services that could be paid to third parties, like appraisals, credit reports, title searches, and property surveys, are often excluded . These costs still come out of your pocket, but because they are not paid directly to the lender, they do not factor into the APR calculation.

Fixed APR Versus Variable APR

APR comes in two main varieties, and knowing which one you have matters for your financial planning.

A fixed APR stays the same throughout the life of the loan . If you take out a five-year personal loan with a fixed APR of 10 percent, your rate will not change no matter what happens in the broader economy. This predictability makes budgeting easier because you always know what your payment will be.

A variable APR, also called a floating APR, can change over time . These rates are tied to an underlying index, such as the prime rate or the Secured Overnight Financing Rate. When that benchmark moves up or down, your APR moves with it. Variable APRs are common on credit cards and some mortgages, particularly adjustable-rate mortgages. The initial rate on a variable APR loan is often lower than comparable fixed-rate offers, but it carries the risk of increasing in the future .

How APR Affects Your Monthly Payments

Your monthly payment is calculated using your interest rate, not your APR . This confuses many borrowers who assume the APR determines their payment amount. The interest rate sets your actual payment, while the APR tells you the total cost including fees spread across the loan term.

However, APR still affects your monthly obligations indirectly. When fees are added to your loan balance rather than paid upfront, you pay interest on those fees over time. This increases your total debt and can slightly raise your monthly payment compared to a loan with no fees but a slightly higher interest rate.

For short-term loans or loans you plan to pay off quickly, the APR may matter less than the total dollar cost . A loan with a high APR but very short term might cost you less in actual dollars than a loan with a moderate APR stretched over many years. This is particularly relevant for small business financing or bridge loans where the borrowing period is measured in months rather than years.

Zero Percent APR Offers: What to Watch For

Zero percent APR offers sound too good to be true, and in some ways they are. These promotions, common on store credit cards and some personal loans, allow you to borrow without paying interest for a set period, typically twelve to eighteen months .

The catch is what happens when that period ends. If you have not paid off the entire balance by the deadline, interest often starts accruing on the remaining amount, sometimes at a much higher rate than you would have paid originally. Some cards even charge deferred interest, meaning they go back and charge interest on the entire original amount from the purchase date .

Zero percent APR can be a useful tool if you have a clear repayment plan and the discipline to execute it. But for ongoing borrowing or balances you cannot pay quickly, the post-promotion APR matters far more than the introductory rate.

Using APR to Make Smarter Borrowing Decisions

Now that you understand what APR is, how can you use this knowledge to save money? The answer lies in comparison shopping and asking the right questions.

When you receive loan offers from multiple lenders, compare the APRs rather than just the interest rates . This levels the playing field and shows you which loan truly costs less. Be sure you are comparing the same type of APR, fixed to fixed and variable to variable, and that you understand what fees are included in each calculation.

Consider how long you plan to keep the loan. If you expect to sell a home or refinance a loan within a few years, the interest rate may matter more than the APR because you will not pay the fees spread over the full loan term . A loan with lower upfront fees but a slightly higher rate could make more sense for short-term situations.

Check your credit score before applying. Borrowers with excellent credit typically qualify for the lowest APRs, while those with lower scores face higher rates . Taking time to improve your credit before borrowing can save you thousands over the life of a loan.

The Bottom Line on APR

APR exists to protect you, the borrower, by forcing lenders to disclose the true cost of credit in a standardized way. It is not a perfect measure, and it does not include every possible fee or account for how quickly you might repay a loan. But it remains the best single number for comparing borrowing options and understanding what a loan will really cost.

The next time you see an APR on a credit card offer or loan advertisement, you will know exactly what it represents: the total annual cost of borrowing, including interest and fees, wrapped into one percentage. Armed with this knowledge, you can shop smarter, borrow more strategically, and keep more of your money where it belongs, in your pocket.

Image Prompts for This Article

Prompt: A split-screen comparison showing two identical piggy banks. On the left, a label reads “Interest Rate 6%” with only a few coins inside. On the right, a label reads “APR 7.2%” with the same piggy bank filled higher to show hidden fees as additional coins. Clean, educational illustration style with soft lighting and a white background.

Prompt: A close-up photograph of a loan estimate document on a wooden desk. A person’s hand is using a yellow highlighter to mark the APR section. A calculator, reading glasses, and a cup of coffee are visible nearby. Warm, natural lighting suggesting a home office environment.

Prompt: A visual metaphor showing two identical price tags on different loans. The first tag shows only the interest rate price. The second tag shows the APR price with a magnifying glass revealing hidden fees like origination, processing, and insurance costs written in smaller print underneath. Modern flat design style with a clean, professional look.

Leave a Reply