If you are among the millions of Americans carrying student loan debt, you have likely heard the term “refinancing” thrown around as a potential solution for lowering your monthly payments or saving money over the life of your loan. With interest rates fluctuating and the job market remaining competitive, 2026 presents a unique landscape for borrowers looking to take control of their educational debt. Student loan refinancing companies offer a pathway to potentially secure a lower interest rate, reduce your monthly payment, or simply simplify your finances by consolidating multiple loans into a single monthly bill. However, navigating the myriad of lenders requires a clear understanding of what each offers and whether refinancing aligns with your long-term financial goals.

Understanding the Refinancing Landscape in 2026

Before diving into specific lenders, it is important to understand what refinancing actually entails. When you refinance, a private lender pays off your existing student loans—whether they are federal, private, or a mix of both—and issues you a brand new loan with new terms. This new loan ideally comes with a lower interest rate, which can translate to significant savings over time.

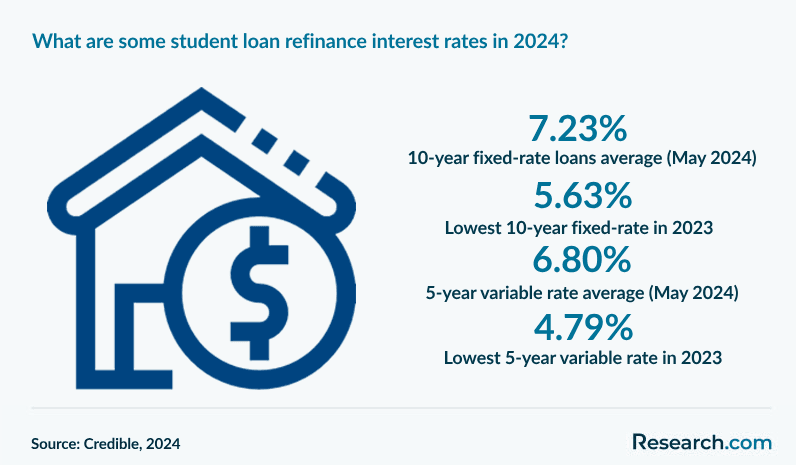

As of early 2026, the market is characterized by intense competition among lenders, which benefits borrowers. According to Bankrate, refinance rates currently start just below 4 percent for the most creditworthy applicants, with fixed rates generally ranging from about 4 percent to nearly 14 percent depending on your credit profile. This wide range underscores the importance of shopping around and comparing offers from multiple student loan refinancing companies before committing.

Top Student Loan Refinancing Companies for 2026

The market is filled with excellent options, each catering to slightly different borrower needs. Here are some of the most compelling student loan refinancing companies available this year.

SoFi: Best for Member Perks and Community

SoFi has long been a dominant force in the refinancing space, and for good reason. This lender offers competitive rates starting at 4.24% fixed APR and 5.99% variable APR, with terms ranging from five to twenty years. What truly sets SoFi apart, however, is its emphasis on community and career support. Borrowers gain access to free career coaching, wealth management advisors, and exclusive member events.

SoFi also offers unemployment protection, which pauses your payments and provides job placement assistance if you lose your job through no fault of your own. There are no fees of any kind—no origination fees, no late fees, and no prepayment penalties. For borrowers who value a holistic financial relationship, SoFi is an outstanding choice among student loan refinancing companies.

Earnest: Best for Customization and Flexibility

If you value control over the fine print of your loan, Earnest deserves a close look. Earnest offers fixed rates starting at 4.15% APR and variable rates starting at 5.88% APR when you enroll in autopay. The company is known for its precision-based underwriting, which considers not just your credit score but also your spending habits and saving patterns.

The hallmark feature of Earnest is the ability to customize your loan term down to the exact month, rather than being locked into standard five-year increments. You can choose any repayment period from five to twenty years, allowing you to fine-tune your monthly payment to fit your budget perfectly. Additionally, Earnest allows you to skip one payment per year after you have made six consecutive on-time payments, providing a rare flexibility that can be a lifesaver during the holidays or an unexpected expense.

RISLA: Best for Borrower Protections

For borrowers who are concerned about losing the safety nets associated with federal loans, the Rhode Island Student Loan Authority offers a compelling compromise. RISLA is a non-profit lender that provides fixed-rate refinancing starting at 3.99% APR, with terms of five, ten, or fifteen years.

What makes RISLA stand out among student loan refinancing companies is its commitment to borrower protections. It is one of the few private lenders to offer income-based repayment plans, allowing you to adjust your payments based on your earnings if you hit a rough patch. It also provides up to twenty-four months of forbearance in cases of economic hardship. For borrowers with federal loans who are hesitant to give up protections but still want a lower rate, RISLA offers a rare bridge between the private and public worlds.

EdvestinU: Best for Non-Graduates

Not everyone who holds student debt finished their degree, but that does not make the debt any less real. EdvestinU stands out as a lender that is willing to work with borrowers who did not complete their academic programs. This inclusive approach opens the door to refinancing for a group that is often overlooked by other lenders.

EdvestinU offers fixed rates ranging from 4.15% to 9.06% APR, with loan terms from five to fifteen years. Borrowers need a minimum credit score of 700 and at least $30,000 in annual income to qualify. For those who meet these requirements, EdvestinU provides a pathway to potentially lower rates and simplified repayment, even without a diploma in hand.

College Ave: Best for Speed and User Experience

College Ave has built a reputation for its streamlined, intuitive application process that can be completed in just three minutes with an instant credit decision. The lender offers competitive rates, with variable APRs starting at 3.89% and fixed APRs starting at 2.84% according to recent data, though rates fluctuate based on market conditions.

College Ave provides multiple repayment term options ranging from five to twenty years and allows borrowers to choose between fixed and variable rates. Importantly, there are no application fees, and the company is known for its transparent pricing and excellent customer service. A notable development in early 2026 is College Ave’s expanded partnership with credit unions like Suncoast Credit Union, making its refinancing products available to an even wider audience through trusted local institutions.

Credit Unions: The Hidden Gems in Refinancing

While national online lenders often dominate the conversation, credit unions across the country offer competitive refinancing options that deserve consideration. These member-owned institutions frequently provide lower rates and more personalized service than their for-profit counterparts.

For example, 3Rivers Federal Credit Union offers student loan refinancing with fixed rates ranging from 6.54% to 7.54% APR depending on the term length, with loan amounts starting at $5,000. While these rates may not be the absolute lowest on the market, credit unions often compensate with superior customer service and a community-focused approach.

Similarly, the partnership between Suncoast Credit Union and College Ave demonstrates how traditional credit unions are leveraging fintech partnerships to offer best-in-class refinancing products to their members. If you already have a relationship with a credit union, it is always worth checking what refinancing options they offer before looking elsewhere.

The Critical Decision: Federal vs. Private Loans

Before you refinance with any of these student loan refinancing companies, it is essential to understand what you stand to lose. If you refinance federal student loans with a private lender, you forfeit all federal protections permanently. This includes access to income-driven repayment plans, Public Service Loan Forgiveness, generous deferment and forbearance options, and potential future forgiveness programs that Congress might create.

This is not a decision to take lightly. As Saving for College emphasizes, while federal consolidation will not lower your interest rate, it preserves these valuable benefits. The general rule of thumb is to only refinance federal loans if you are absolutely certain you will not need these protections and the interest rate savings are substantial enough to justify the risk.

For private loans, however, there is no such downside. Private loans do not come with federal protections, so refinancing them is a straightforward financial calculation: if you can qualify for a lower rate, it almost always makes sense to do so.

How to Choose the Right Refinancing Company

With so many excellent options available, selecting the right partner requires some introspection. Start by checking your credit score. Most student loan refinancing companies reserve their lowest rates for borrowers with scores in the high 600s or 700s. If your credit needs work, it may be worth waiting and improving your score before applying.

Next, take advantage of pre-qualification tools. Nearly every lender on this list allows you to check your rate with a soft credit pull that will not impact your credit score. Get quotes from at least three different lenders to compare not just the interest rate, but also the repayment terms, borrower benefits, and customer service reputation.

Consider your need for flexibility. Do you want the ability to skip a payment occasionally? Earnest excels there. Do you want ironclad borrower protections? RISLA is your best bet. Do you value career support and a sense of community? SoFi is unmatched.

Finally, read the fine print regarding fees. The lenders featured here generally charge no origination fees or prepayment penalties, but not all lenders are so generous. Ensure you understand the total cost of the loan before signing.

Conclusion

The landscape of student loan refinancing companies in 2026 is rich with options, from the customization of Earnest and the community focus of SoFi to the protective features of RISLA and the inclusive policies of EdvestinU. By taking the time to understand your own financial situation, comparing multiple offers, and carefully weighing the decision to refinance federal loans, you can potentially save thousands of dollars and gain greater control over your financial future. The key is to approach the decision not as a simple transaction, but as a strategic move in your broader financial life.

Leave a Reply