The ads are everywhere. “Consolidate your debt into one low monthly payment!” “Reduce your interest rates and get out of debt faster!” “Bad credit? No problem!” With promises this appealing, it is natural to wonder whether debt consolidation is a legitimate financial tool or just another trap for struggling borrowers.

The truth, as with most financial products, lies somewhere in the middle. Debt consolidation is not inherently a scam. It is a legitimate strategy that has helped millions of Americans simplify their finances and save money on interest. But the industry is also riddled with scammers who prey on vulnerable consumers, and even legitimate consolidation can backfire if you do not understand how it works.

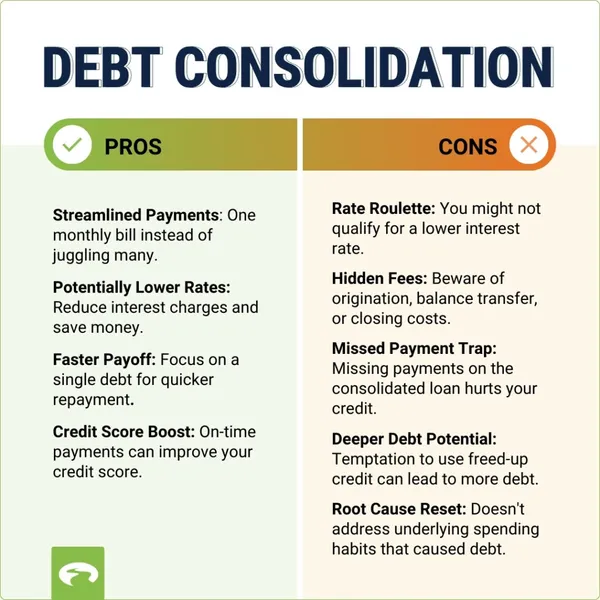

When Debt Consolidation Is Legitimate

Debt consolidation simply means taking out a new loan to pay off multiple existing debts. When done correctly, you end up with a single monthly payment, ideally at a lower interest rate than what you were paying across your credit cards.

This approach makes sense in specific situations. If you have decent credit and can qualify for a personal loan with a single-digit interest rate, swapping out credit card debt at twenty-two percent or higher saves you significant money over time. Balance transfer credit cards offering zero percent interest for twelve to twenty-one months provide another legitimate path, giving you a window to pay down principal without accruing new interest.

The key is that legitimate consolidation comes from reputable lenders who earn money through interest, not from upfront fees. Banks, credit unions, and established online lenders like SoFi or Discover fall into this category. They check your credit, verify your income, and lend based on their assessment of your ability to repay.

When Consolidation Becomes a Scam

The dark side of debt consolidation involves companies that pose as helpers while actually making your situation worse. These operations share recognizable warning signs.

Upfront fees top the list of red flags. Legitimate lenders may charge origination fees, but these are typically deducted from your loan amount after approval, not demanded before you receive funds. Scammers ask for processing fees, application fees, or “first month’s payment” upfront, then disappear with your money.

Guaranteed approval regardless of credit history signals trouble. Every legitimate lender evaluates your ability to repay. Claims of “no credit check” approvals usually mean exorbitant interest rates or outright fraud.

Unsolicited offers by phone or text message violate federal law. Legitimate lenders do not cold-call potential customers. If someone reaches out to you offering debt consolidation, hang up.

Requests for wire transfers or prepaid debit cards should end the conversation immediately. These payment methods are untraceable and favored by scammers. Legitimate lenders use secure payment channels.

The Strategic Financial Solutions Case: A Warning

One of the largest debt relief fraud cases in recent history illustrates exactly how these scams operate. In January 2024, the Consumer Financial Protection Bureau and seven state attorneys general sued Strategic Financial Solutions, a debt-relief enterprise that had allegedly swindled more than $100 million from financially struggling families.

The scheme worked like this: SFS used advertisements to target vulnerable consumers, promising loans that would help pay down debts. When consumers called, they were told they did not qualify for the advertised loans but were instead encouraged to enroll in SFS’s debt-relief services. The company promised that its network of law firms would negotiate lower debt amounts.

Instead, SFS required customers to make immediate payments into escrow accounts, then collected hefty fees long before settling any debts. The law firm involvement was a facade; non-lawyer SFS employees handled whatever negotiations actually occurred. Consumers ended up worse off while SFS executives lined their pockets.

Consumer Reports later detailed the experience of Sally Proske, who paid more than $16,000 to SFS over three years, only to see about half that amount actually go to her creditors. Her credit score remained in the low 500s. Another client, Adam Schnakenberg, paid nearly $30,000 in fees and still faced wage garnishment from a creditor.

When Consolidation Backfires Even Without Scams

You do not need to encounter an outright scam for debt consolidation to fail you. Even legitimate consolidation backfires when the underlying behavior does not change.

The Ramsey Show featured a couple in their seventies who had been completely debt-free after completing Financial Peace University in 2016. They had paid off everything and even bought their mobile home with cash. But by 2025, they owed $46,000 across thirteen credit cards and three personal loans.

Their income consisted entirely of Social Security: $1,600 from her, $1,500 from him. They lived in expensive Riverside County, California, and simply could not make the numbers work. When they called for advice about a $29,000 debt consolidation loan they had been approved for, Dave Ramsey’s response was blunt: “You cannot borrow your way out of debt”.

The problem was not the consolidation offer itself. The problem was the pattern. As Ramsey explained, “The pattern keeps you spending more than you have coming in.” Consolidation would only rearrange the debt, not solve the underlying gap between income and expenses.

A bankruptcy attorney shared another cautionary tale about a retired woman on Social Security who enrolled with a debt consolidation company. She stopped making minimum payments as instructed, paid a deposit, and waited. Months later, creditors had never been contacted. The company refused to cancel or return her deposit and kept trying to withdraw funds from her bank account. Her credit was ruined, and she ultimately filed Chapter 7 bankruptcy.

How to Consolidate Safely

If you decide consolidation makes sense for your situation, follow these guidelines to protect yourself.

Start with nonprofit credit counseling. Before taking out any loan, meet with a counselor from a NFCC-affiliated agency. They can help you explore all options, including debt management plans that may lower your interest rates without new loans.

Contact your creditors directly. Many credit card companies will work with you directly to lower payments or change due dates. They would rather receive reduced payments than none at all.

Research lenders thoroughly. Check state registration, Better Business Bureau ratings, and verified customer reviews. Verify physical addresses and call customer service numbers to ensure real people answer.

Compare multiple offers. Legitimate consolidation requires shopping around. Get quotes from several lenders and compare APR, fees, and repayment terms. Be wary of any lender that pressures you to decide immediately.

Read every word of the contract. Ensure you understand the interest rate, whether it is fixed or variable, the repayment term, any prepayment penalties, and all fees. If something differs from what you discussed, ask questions.

Have a plan beyond the loan. Consolidation only works if you stop accumulating new debt. Cut up credit cards, create a budget, and address the spending habits that created the problem initially.

The Bottom Line

Debt consolidation is not a scam, but the industry is full of scammers. Legitimate consolidation through reputable lenders can simplify payments and reduce interest costs. But it only works when combined with changed behavior and realistic budgeting.

Before signing anything, ask yourself whether you are treating the symptom or the disease. If your problem is high interest rates, consolidation may help. If your problem is spending more than you earn, consolidation will only delay the inevitable.

As Ramsey told the California couple, “You cannot borrow your way out of debt.” The math must change, not just the monthly payment.

Leave a Reply