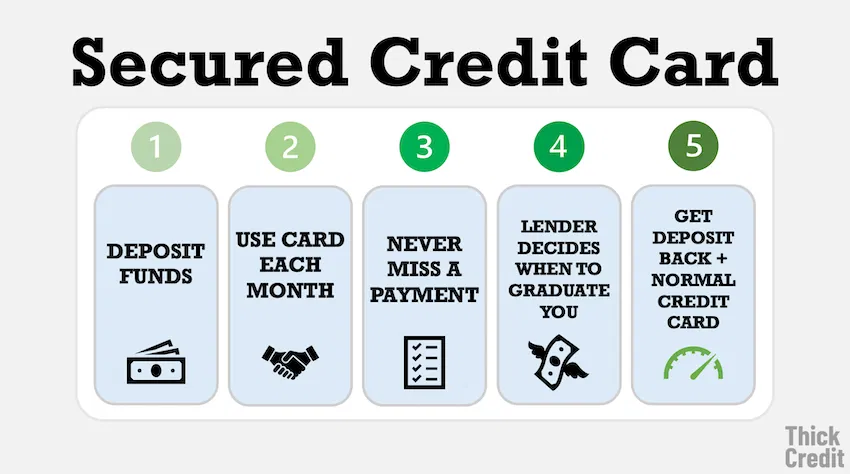

You made the smart decision to start with a secured credit card. You put down your deposit, used the card responsibly, and watched your credit score climb. Now you are ready for the next step: leaving the training wheels behind and getting your security deposit back while keeping your credit history intact.

Graduating from a secured card to an unsecured card represents a major milestone in your financial journey. It means the issuer trusts you enough to extend credit without requiring collateral upfront. Your deposit returns to you, your credit line may increase, and you gain access to better rewards and benefits. But graduation does not happen automatically. You need to understand how the process works and what you can do to make it happen faster.

What Graduation Actually Means

When you graduate from a secured card, your account converts to an unsecured line of credit. The issuer returns your security deposit, either as a statement credit, a check, or a direct deposit to your bank account. Your credit limit may stay the same, increase, or occasionally decrease depending on the issuer’s policies.

Crucially, graduation is not the same as closing your secured card and opening a new unsecured card. When your account converts, you keep the same account number and the same credit history. That history continues to age and benefit your credit score. If you closed the secured card and opened a new one, you would lose that history and start over.

Most major issuers review secured card accounts periodically for graduation. Discover begins reviewing accounts after seven months of responsible use. Capital One starts reviews at six months. Other issuers may wait twelve months or longer. The review considers your payment history, your credit utilization, and your overall credit profile.

Step One: Establish a Pattern of Responsible Use

Graduation requires proof that you can handle credit responsibly. That proof comes from consistent behavior over time, not just a single month of perfect payments.

Pay every bill on time, every single month. Payment history carries the most weight in credit scoring, and issuers want to see that you can be trusted to pay as agreed. One late payment can reset your graduation timeline or eliminate your chances entirely.

Keep your balance low relative to your credit limit. Using too much of your available credit signals risk, even if you pay in full each month. Aim to keep your reported utilization below thirty percent, and ideally below ten percent, on your secured card.

Use the card regularly. An account that sits unused does not demonstrate your ability to manage credit. Small recurring charges like streaming subscriptions or gas purchases keep the account active without creating high balances.

Step Two: Understand Your Issuer’s Graduation Policy

Not all secured cards graduate on the same timeline or using the same criteria. Knowing your issuer’s specific policies helps you set realistic expectations.

Discover it Secured cardholders qualify for automatic account reviews starting at seven months. Discover looks for responsible use and may graduate your account, return your deposit, and sometimes increase your credit limit without any action on your part.

Capital One reviews secured accounts at around six months for potential graduation. Their policy varies by individual card product, but consistent on-time payments and responsible use generally lead to graduation offers.

Citi Secured Mastercard requires eighteen months of on-time payments before you become eligible for graduation. This longer timeline makes Citi a slower option for those seeking quick progress.

U.S. Bank Secured Visa reviews accounts periodically but does not publish specific timelines. Cardholders report graduation occurring anywhere from twelve to twenty-four months after account opening.

If your issuer offers online account access, look for information about graduation policies in the terms or frequently asked questions. When in doubt, calling customer service and asking directly about graduation eligibility provides the clearest answer.

Step Three: Monitor Your Credit Progress

While you wait for graduation, tracking your credit score helps you understand how you are progressing. Most secured card issuers provide free credit score access as a cardholder benefit.

Discover includes your FICO Score 8 on every monthly statement. Capital One offers CreditWise, which provides your VantageScore 3.0. These tools let you see the impact of your responsible behavior and confirm that your efforts are paying off.

Watching your score also helps you identify problems early. If your score drops unexpectedly, you can investigate and address the issue before it affects your graduation chances. Regular monitoring keeps you connected to your financial progress.

Step Four: Consider Requesting Graduation

Some issuers require you to request graduation rather than offering it automatically. If your card has no published graduation timeline or if you believe you qualify based on your history, reaching out proactively can move things forward.

Call the number on the back of your card and ask to speak with someone about converting your secured account to unsecured. Explain that you have used the card responsibly, paid on time, and maintained low balances. Ask whether you qualify for graduation and what steps are required.

If the representative says you do not yet qualify, ask what specific criteria you need to meet and when you should check again. This information gives you a clear target to work toward rather than guessing about expectations.

Some issuers may require you to apply for a new unsecured card rather than converting your existing account. If this happens, ask whether you can keep your secured card open after approval to preserve its credit history. Closing the secured card immediately would remove its positive history from your credit file.

Step Five: Prepare for the Hard Inquiry

When you request graduation, some issuers may perform a hard inquiry on your credit report to evaluate your eligibility. This inquiry can temporarily lower your score by a few points, but the long-term benefit of graduation outweighs this minor and temporary dip.

If you are planning a major credit application like a mortgage or auto loan in the near future, timing matters. You may want to wait until after that application to pursue graduation, or ask the issuer whether they can use a soft inquiry instead.

Knowing your credit score before requesting graduation helps you assess your chances. If your score has improved significantly since opening the secured card, you are in a strong position. If your score remains low, waiting a few more months to build history makes sense.

Step Six: Handle Your Deposit Return

When graduation happens, your security deposit comes back to you. The method varies by issuer but typically involves one of three approaches.

Some issuers apply the deposit as a statement credit, effectively paying down any balance you carry and returning the remainder as available credit. Others mail a check to your address on file. Many now offer direct deposit to your linked bank account.

If you have moved since opening the card, ensure your address and bank information are current in the issuer’s system. A returned check or failed deposit delays your access to funds that rightfully belong to you.

Do not close your secured card immediately upon receiving your deposit back. The account now appears as unsecured on your credit report, and its history continues to benefit your score. Keep it open and use it occasionally to prevent inactivity closures.

Step Seven: Celebrate and Plan Next Steps

Graduation marks real financial progress, and you should acknowledge that achievement. You started with a product designed for those building or rebuilding credit, and you proved you could handle it responsibly. Your deposit returns, your credit line may increase, and you gain access to better financial products.

But graduation is not the finish line. Now you can consider adding another card with better rewards, requesting credit limit increases on existing accounts, or exploring other credit products that match your improved profile.

Apply for new credit strategically rather than all at once. Space applications at least six months apart to avoid multiple hard inquiries clustering together. Research cards that offer rewards aligned with your spending patterns.

Continue the habits that earned you graduation. Pay every bill on time, keep balances low, monitor your credit regularly. These behaviors built your success, and they will sustain it.

What If Your Issuer Does Not Offer Graduation?

Some secured cards, particularly those from smaller issuers or those designed specifically for credit building, may not offer graduation at all. If your card falls into this category, your path forward looks different.

After twelve to eighteen months of responsible use, consider applying for an unsecured card from a different issuer. Your improved credit profile should qualify you for better options. Once approved, you can keep your secured card open or close it depending on whether it charges an annual fee.

If your secured card has no annual fee, keeping it open adds to your available credit and contributes to your account age. If it charges a fee, closing it after obtaining new unsecured cards makes financial sense.

Common Mistakes to Avoid

The graduation process trips up some cardholders who make avoidable errors.

Carrying high balances in the months before expected graduation signals risk and may delay or prevent conversion. Keep utilization low consistently, not just when you first opened the card.

Applying for multiple new cards while waiting for graduation creates hard inquiries and new accounts that make your credit profile look riskier temporarily. Space applications thoughtfully.

Closing your secured card immediately after graduation removes its positive history from your credit file. Keep it open and let it continue benefiting your score.

Ignoring your credit report means you might miss errors that could affect graduation decisions. Check your reports regularly at AnnualCreditReport.com and dispute any inaccuracies.

The Bottom Line

Graduating from a secured card to an unsecured card represents a significant achievement in your credit journey. The process requires patience, consistency, and understanding of how your specific issuer handles conversions.

Start by establishing six to twelve months of perfect payment history with low utilization. Learn your issuer’s graduation policies and timeline. Monitor your credit progress. When the time feels right, ask about graduation or wait for automatic review.

When your deposit returns and your account converts, celebrate your progress and plan your next financial moves. You have proven you can handle credit responsibly. Now use that foundation to build the financial life you deserve.

Leave a Reply