The question seems simple enough: how many credit cards do you actually need to achieve the best possible credit score? Walk into any wallet and you will find answers ranging from “just one” to “as many as you can handle.” The truth is that there is no magic number, but understanding how card count influences your score helps you make the right decision for your unique situation.

The average American carries about four credit cards, according to Experian data. Some people achieve perfect 850 scores with only two cards, while others maintain excellent credit with ten or more. The number matters far less than how you manage the cards you have.

How Credit Card Count Affects Your Score

Your credit score does not directly reward you for having a specific number of cards. Instead, the number of cards influences the major scoring factors in ways that can help or hurt depending on your habits.

Credit Utilization: The Mathematics of Multiple Cards

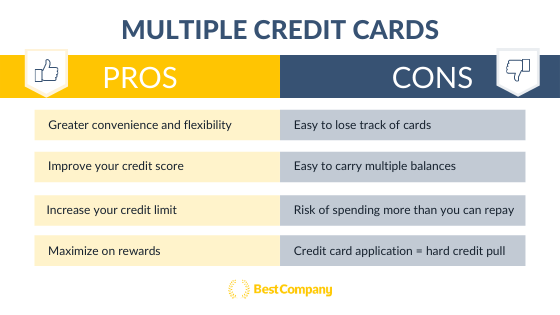

The most significant way multiple cards help your score is through credit utilization, which accounts for 30% of your FICO score. This factor measures your total balances divided by your total available credit. More cards mean more available credit, which can dramatically lower your utilization if you keep your spending constant.

Consider this example from credit expert John Ulzheimer, who learned this lesson the hard way. He initially had only one credit card with a $600 limit and was frequently maxing it out, which destroyed his utilization ratio. By opening additional cards, he increased his available credit and significantly improved his score.

The math works like this. With one card at a $5,000 limit and a $2,500 balance, your utilization sits at 50%, well above the recommended threshold. With three cards offering a combined $15,000 limit and the same $2,500 total balance, your utilization drops to about 17%, which looks much better to scoring models.

Even if you pay in full each month, the timing of balance reporting matters. Card issuers typically report your balance on statement closing dates, not payment due dates. Having multiple cards allows you to spread spending across accounts, keeping individual card utilization low even before you make payments.

Payment History: More Responsibility, More Risk

Payment history carries 35% of your FICO score, making it the single most important factor. Here, more cards create more responsibility. Every card requires on-time payment, and missing just one can devastate your score regardless of how many other cards you manage perfectly.

If you struggle to track due dates, additional cards multiply your risk. Setting up automatic payments for at least the minimum amount due on every card eliminates this danger entirely.

Credit Age: The Long Game

The length of your credit history contributes 15% to your score. Opening new cards lowers your average account age temporarily, which can cause small, short-term score drops. However, those new cards eventually age and contribute positively to your history.

This is why keeping old cards open matters enormously. Even if you rarely use your first credit card, keeping it active maintains its contribution to your credit age and total available credit.

Credit Mix: Variety Over Volume

Credit mix accounts for 10% of your score and rewards having different types of credit, not just multiple cards. A mortgage or auto loan alongside your credit cards helps more than ten cards alone. But at minimum, having at least one credit card in your name benefits this category.

New Credit: Application Spacing Matters

Each credit card application triggers a hard inquiry, which can knock up to five points off your score temporarily. Multiple applications in a short period compound this effect and signal risk to lenders. Spacing applications at least six months apart minimizes this impact.

Finding Your Optimal Number

Given these factors, how do you decide how many cards work for you?

The Minimum: Start with One

If you are new to credit or rebuilding, start with one well-chosen card. This builds payment history and establishes a foundation. A single card with responsible use can generate an excellent score over time.

However, a thin credit file with only one or two accounts may limit you. Some lenders consider anyone with fewer than five accounts a “thin-file” consumer, which can affect approval decisions. Adding a second card after six to twelve months of responsible use thickens your file and provides backup if the first card is lost or compromised.

The Sweet Spot: Two to Four Cards

For most people, two to four cards strike the right balance. This allows you to:

- Maintain healthy total available credit

- Keep utilization low across accounts

- Diversify rewards for different spending categories

- Build a buffer without creating management chaos

With this setup, you might have a flat-rate cash back card for everyday spending, a category card for groceries or dining, and perhaps a travel card for trips.

The Upper End: Five or More

Some credit enthusiasts maintain ten or more cards with excellent scores. This works only if you:

- Track all due dates religiously (automatic payments essential)

- Keep spending under control across accounts

- Understand the purpose of each card

- Manage annual fees without losing value

The risk with many cards is not the score impact itself, but the increased chance of missed payments or overspending.

When Multiple Cards Backfire

More cards hurt your score in specific situations. If you carry balances across multiple cards, you may end up with high total utilization that negates the benefit of higher limits. If you open several cards within months, the hard inquiries and lowered average age temporarily depress your score.

The biggest danger is behavioral. More credit limits can tempt overspending, and if you cannot pay those balances, the resulting high utilization and potential missed payments destroy the very score you sought to build.

Strategic Considerations

When deciding whether to add a card, consider these factors.

Rewards optimization often justifies multiple cards. Using a 5% card for groceries and a 2% card for everything else earns more than a single 1.5% card. But only if the rewards outweigh any annual fees.

Network acceptance matters. Having cards on different networks (Visa, Mastercard, Discover, American Express) ensures you always have a working card regardless of merchant acceptance.

Account age favors keeping old cards open. Even if you stop using a card, keeping it active (perhaps with a small recurring charge) preserves its contribution to your credit history.

The Bottom Line

The number of credit cards that maximizes your score is whatever number you can manage perfectly. For most people, two to four cards provide optimal benefits without excessive complexity. A single card can build excellent credit over time, while a dozen can work for highly organized individuals.

What matters most is never missing payments and keeping balances low across all accounts. Whether you carry two cards or ten, those two habits determine your score far more than the count itself. Choose cards that serve your spending needs, set up automatic payments, and let time do the rest.

Leave a Reply