The phone rings at dinner time. Again. A letter arrives demanding payment for a debt you barely recognize. The stress builds with each contact, and you wonder if you have any power to push back. You do. The debt validation letter is one of the most effective tools in consumer law, and when used correctly, it can make aggressive collectors vanish almost overnight.

Understanding how this tool works, what it requires, and when to use it transforms you from a powerless target into someone who knows their rights. The Fair Debt Collection Practices Act gives you specific protections, and the debt validation letter activates those protections immediately.

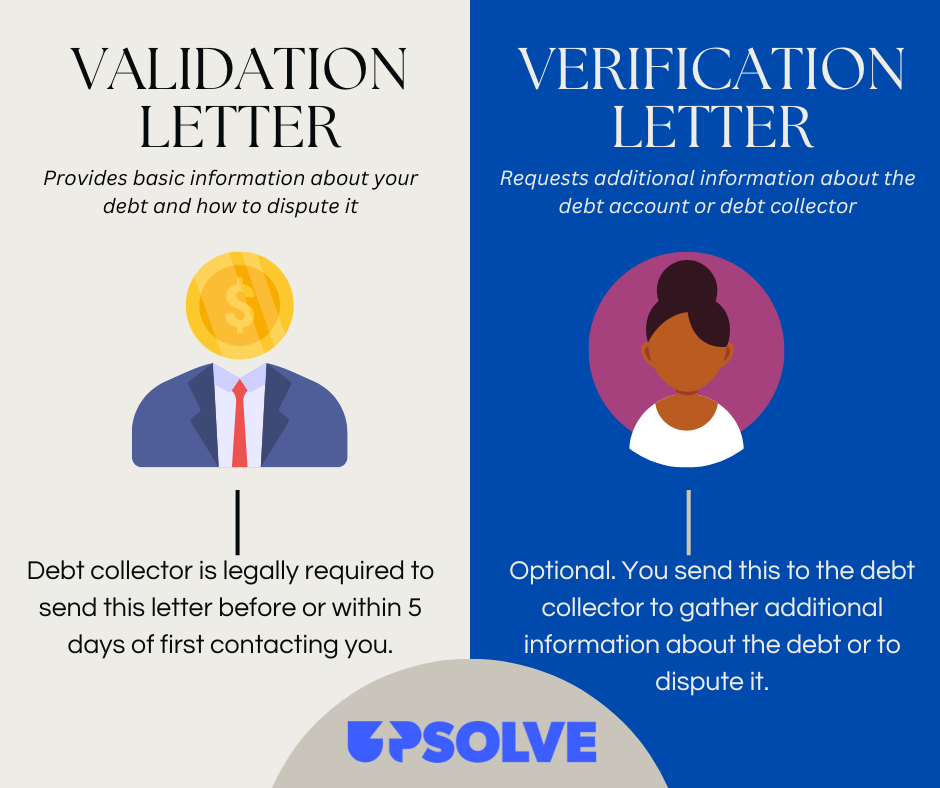

What a Debt Validation Letter Actually Does

A debt validation letter is a formal request asking a debt collector to prove that you actually owe the debt they are trying to collect. Under the Fair Debt Collection Practices Act, collectors must provide verification of the debt or stop collection efforts entirely.

This is not the same as disputing the debt online or over the phone. A written validation letter triggers specific legal obligations. Once the collector receives your letter, they must cease all collection activities until they provide you with proof that the debt is legitimate and that they have the right to collect it.

If they cannot provide proper validation within thirty days, they must stop contacting you permanently and cannot continue trying to collect. Many collectors simply give up at this point because they lack the documentation required to proceed.

When to Send a Debt Validation Letter

Timing matters enormously with validation letters. You have a limited window to exercise your strongest rights.

After a debt collector first contacts you, they must send you a written notice within five days containing specific information about the debt. This notice must include the amount owed, the name of the original creditor, and a statement of your right to dispute the debt.

You then have thirty days from receiving that notice to send your debt validation letter. If you send it within this window, the collector must stop all collection activities until they provide verification. This thirty-day window is your best opportunity to force the collector to prove their case.

If you miss this window, you can still send a validation letter, but the collector is not legally required to stop collection while they investigate. They may continue calling and sending letters even as they work on your request.

What to Include in Your Debt Validation Letter

A proper debt validation letter needs specific elements to be effective. Keep it simple, factual, and professional.

Start with your name, address, and the date. Include the collector’s name and address, along with any account number or reference number they provided in their notice.

Clearly state that you are disputing the debt and requesting validation. Include language like: “I dispute this debt in its entirety and request validation pursuant to the Fair Debt Collection Practices Act.”

Request specific documentation. Ask for proof that the collector owns the debt or has authority to collect it. Request a copy of the original contract or agreement showing your signature. Ask for a complete accounting of how the debt amount was calculated, including all fees and interest added.

State clearly that collection activities must cease until validation is provided. Remind them that continued contact without validation violates federal law.

Send your letter by certified mail with return receipt requested. This gives you proof of when the collector received your letter, which matters if they violate the law by continuing to contact you.

What Collectors Must Provide

When you request validation, the collector must provide meaningful documentation, not just a computer printout. Courts have generally required collectors to provide actual proof that the debt is yours and that they have the right to collect it.

Proper validation typically includes a copy of the original contract or application bearing your signature. It should show the original creditor’s name and the date the account was opened. The collector must also provide a detailed accounting showing how the current balance was calculated.

If the debt has been sold multiple times, the collector must demonstrate the chain of ownership from the original creditor to the current collector. Without this documentation, they cannot prove they have standing to collect.

Many collectors purchase debts in large portfolios with minimal documentation. When faced with a proper validation request, they often cannot produce the required paperwork and must abandon collection efforts.

What Happens After You Send the Debt ValidationLetter

Once your letter is received, the collector must stop all contact until they provide validation. No phone calls, no letters, no threats. Silence.

If they cannot validate the debt within the required timeframe, they have two choices. They can cease collection permanently and return the debt to the original creditor or sell it to another collector. Or they can continue collection, but doing so violates federal law and gives you grounds to sue.

If they do provide validation, you must decide your next steps. Review the documentation carefully. Look for errors in dates, amounts, or account numbers. Verify that the debt is actually yours and that the amount is correct. If errors exist, you can dispute again or consult a consumer attorney about your options.

Common Mistakes That Weaken Your Letter

Certain mistakes can undermine the effectiveness of your validation request.

Sending the letter after the thirty-day window does not invalidate your request, but it does weaken your position. The collector can continue contacting you while they investigate, making the process more stressful.

Requesting validation verbally by phone accomplishes nothing. The law requires a written request to trigger the collector’s obligations. Always put everything in writing.

Failing to send by certified mail leaves you without proof of delivery. If a collector claims they never received your letter, you have no evidence to dispute them.

Admitting you owe the debt in your letter can create problems. Stick to disputing and requesting validation without acknowledging any obligation to pay.

When Collectors Violate the Law

Some collectors ignore validation requests and continue calling anyway. This behavior violates the Fair Debt Collection Practices Act and gives you powerful legal rights.

If a collector contacts you after receiving your validation letter without first providing proper documentation, document every contact. Note dates, times, phone numbers, and what was said. Save voicemails and letters.

You have the right to sue collectors who violate the FDCPA. Successful plaintiffs can recover up to $1,000 in statutory damages plus actual damages and attorney fees. Many consumer attorneys take these cases on contingency, meaning you pay nothing upfront.

The threat of an FDCPA lawsuit often motivates collectors to settle quickly and delete the debt entirely.

Sample Debt Validation Letter

Here is a simple template you can adapt:

[Your Name]

[Your Address]

[Date]

[Collector Name]

[Collector Address]

[Reference Number]

To Whom It May Concern:

I am writing in response to your recent communication regarding an alleged debt referenced above. I dispute this debt in its entirety and request validation pursuant to the Fair Debt Collection Practices Act, 15 U.S.C. § 1692g.

Please provide the following documentation:

Proof that you own this debt or have authority to collect it

A copy of the original contract bearing my signature

A complete accounting of how the current balance was calculated

The name and address of the original creditor

Until you provide this validation, all collection activities must cease. If you cannot validate this debt, please remove it from my credit report permanently and cease all collection efforts.

Sincerely,

[Your Signature]

[Your Printed Name]

The Bottom Line

A debt validation letter is one of the most powerful consumer tools available. It forces collectors to prove their case, stops harassment immediately, and often makes aggressive collectors disappear entirely.

The key is acting quickly. Send your letter within thirty days of first contact using certified mail. Keep copies of everything. Document any violations. And never let collectors intimidate you into paying debts they cannot validate.

You have rights. Use them.

Leave a Reply