You check your credit score through your bank’s mobile app and see a solid 740. A week later, you sign up for a free credit monitoring service, and it shows 715. Then you pull your full credit report and find yet another number. Before panic sets in, you should know that this experience is completely normal and happens to nearly every consumer who takes an active interest in their financial health.

The truth is that you do not have a single credit score. You have dozens of them. Understanding why multiple scores exist and which ones actually matter when you apply for credit will save you from unnecessary worry and help you focus your energy on what truly counts.

There Is No Single Credit Score

The concept of a universal credit score is one of the most persistent myths in personal finance. In reality, credit scores are calculated by analyzing the information in your credit report using specific mathematical formulas called scoring models. Different models can produce different results even when analyzing the same information, and your credit reports themselves can vary from one bureau to another.

Think of it this way: your credit history is like a raw ingredient, and scoring models are different recipes. The same ingredient can yield slightly different dishes depending on which recipe you follow. When lenders check your credit, they choose which recipe to use and which source of ingredients to pull from.

Why Your Scores Differ Across Sources

Several factors contribute to the variations you see when checking your credit from different sources. Understanding these factors demystifies the whole process and helps you interpret the numbers you encounter.

Different Credit Bureaus Have Different Information

The three major credit bureaus—Equifax, Experian, and TransUnion—operate independently of one another. They collect information from lenders, creditors, and public records, but not every lender reports to every bureau. Your credit card company might report your payment history to Experian and TransUnion but not to Equifax. That means your Equifax report could lack positive information that appears on your other reports, potentially resulting in a lower score from that bureau.

Timing also plays a role. Lenders typically report information to the bureaus once per month, but they may do so on different days. A payment you made last week might appear on one bureau’s report immediately while another bureau still shows the old balance. These timing differences can create temporary score variations that usually resolve within a billing cycle.

Different Scoring Models Weigh Factors Differently

FICO and VantageScore are the two main companies that create credit scoring models, and they approach the task with different philosophies. FICO has been around since 1956 and is used by approximately ninety percent of lenders. VantageScore was launched in 2006 as a joint venture between the three credit bureaus and has gained significant ground since then.

Both models consider similar factors, but they assign different weights to each one. Payment history carries the most weight in both systems, but FICO allocates thirty-five percent to this category while VantageScore gives it forty percent. Credit utilization represents thirty percent of a FICO score but only twenty percent of a VantageScore 3.0. These weighting differences mean that the same credit behavior can impact your scores differently depending on which model calculates them.

The models also treat certain situations differently. VantageScore 4.0 ignores paid collection accounts entirely, while some FICO versions still factor them into your score. Late mortgage payments hit harder in VantageScore than late credit card payments, reflecting research about which missed payments most strongly predict future default.

Multiple Versions of Each Model Exist

To further complicate matters, both FICO and VantageScore have released multiple versions of their scoring models over the years. FICO currently has dozens of different score versions in use, including base scores for general lending and industry-specific scores for mortgages, auto loans, and credit cards.

FICO 8 remains the most widely used version for general lending decisions, but many lenders still rely on older versions like FICO 5, 4, and 2 for mortgage applications. FICO 9 and FICO 10T have introduced refinements such as different treatment of medical debt and the incorporation of trended data that looks at your payment patterns over time rather than just a single snapshot.

VantageScore has released four major versions since its inception, with VantageScore 3.0 and 4.0 being the most commonly used today. Each version brings changes to the scoring formula, which means your score can vary depending on which version a lender chooses to access.

Which Credit Scores Lenders Actually Use

The answer to this question depends entirely on what type of loan you are seeking and which lender you choose. Different lending situations call for different scoring models, and lenders have the freedom to select the models they believe best predict risk for their specific portfolios.

For Mortgage Applications

Mortgage lending follows some of the most specific rules when it comes to credit scoring. Most mortgage lenders still rely on what are known as the classic FICO scores: FICO Score 2 from Experian, FICO Score 4 from TransUnion, and FICO Score 5 from Equifax. When you apply for a mortgage, the lender pulls all three of these scores and typically uses the middle score to make their decision.

If you are applying with a co-borrower, the lender looks at both applicants’ middle scores and then uses the lowest of those two numbers for qualification purposes. This lowest-middle-score approach means that joint applicants are only as strong as the weaker credit profile in the pair.

Recent changes in the mortgage industry are expanding the scoring models lenders can use. Starting in 2025, loans backed by Fannie Mae and Freddie Mac can use VantageScore 4.0 alongside the traditional FICO scores, though this change does not apply to government loans like FHA, USDA, or VA mortgages.

For Credit Card Applications

Credit card issuers have more flexibility in which scores they use. Many rely on FICO Bankcard Scores, which are industry-specific versions ranging from 250 to 900 rather than the standard 300 to 850 range. These scores are calibrated specifically to predict credit card repayment behavior.

VantageScore is also popular among credit card issuers, particularly for pre-approval offers and marketing campaigns. Some issuers even develop their own custom scoring models that incorporate FICO or VantageScore as components alongside other data points like your banking history or relationship with the institution.

For Auto Loans

Auto lenders frequently use FICO Auto Scores, another industry-specific variation that ranges from 250 to 900. These scores place different emphasis on factors most relevant to auto lending, such as how you have managed previous installment loans.

Some auto lenders use VantageScore instead of or in addition to FICO scores. The dealership you visit may pull your credit from multiple sources to find the lender and scoring model that offers you the best terms.

For General Monitoring

When you check your credit score through free apps, your bank’s mobile app, or credit monitoring services, you typically see either a FICO 8 score or a VantageScore 3.0 score. These are useful for tracking trends in your credit health, but they may not be identical to the scores your lender will see when you apply for credit.

For example, the score you see in your banking app might be a VantageScore based on your TransUnion report, while your mortgage lender pulls FICO scores from all three bureaus. The number you see gives you a general idea of where you stand, but you should expect the actual score used for lending to differ slightly.

How to Manage Multiple Credit Scores

With all these variations floating around, you might wonder how you can possibly keep track of your credit health. The good news is that you do not need to monitor every single score. All scoring models respond positively to the same fundamental behaviors, so focusing on healthy credit habits will improve all your scores over time.

Focus on What Matters

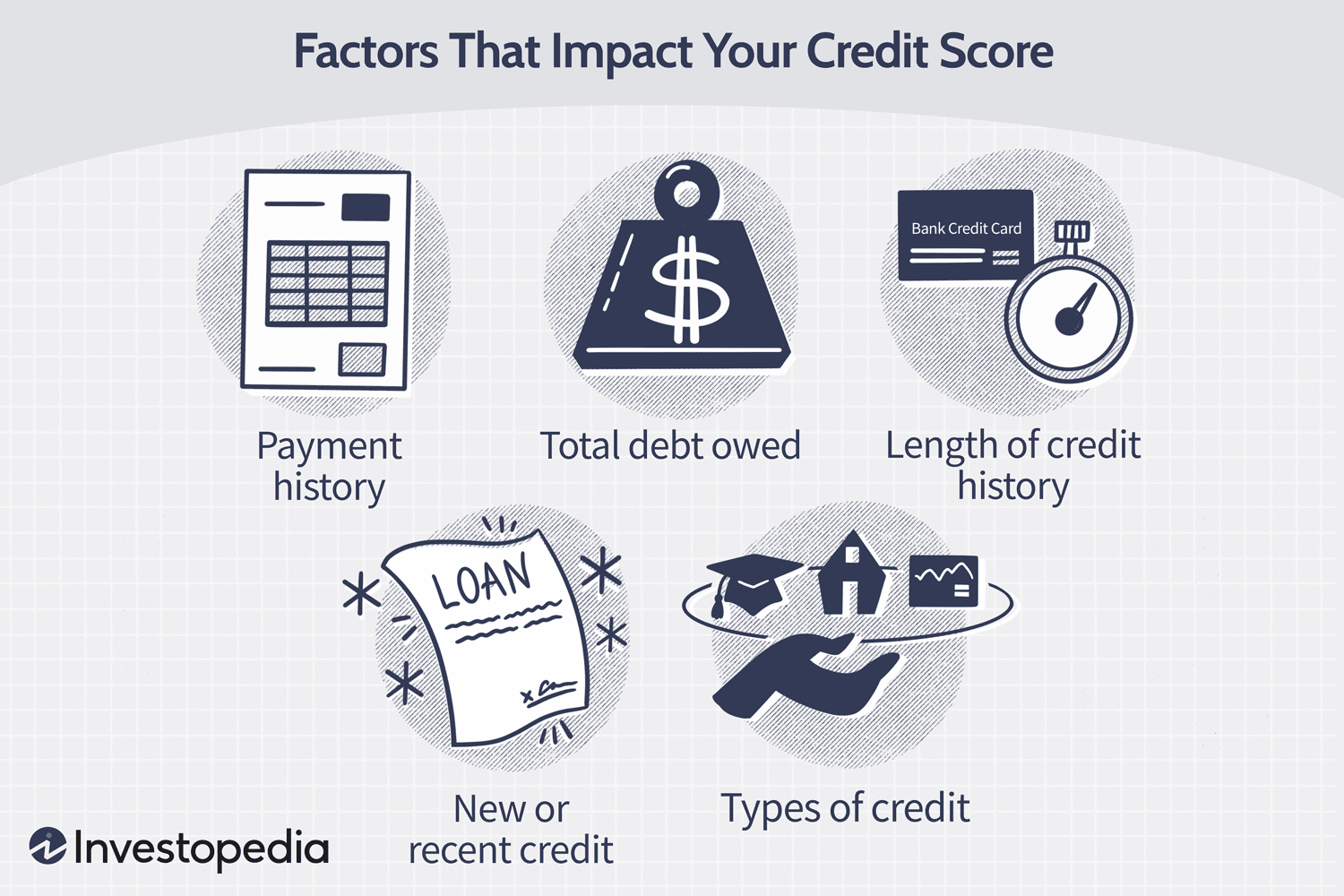

Payment history drives the majority of your scores regardless of which model calculates them. Making every payment on time, every single month, provides the foundation for good credit across all scoring models. Setting up automatic payments for at least the minimum amount due eliminates the risk of accidental late payments.

Credit utilization comes next in importance. Keeping your credit card balances low relative to your credit limits benefits every scoring model, though the exact impact varies. Experts recommend using no more than thirty percent of your available credit at any time, with even lower utilization benefiting you further.

The length of your credit history, your mix of credit types, and how often you apply for new credit round out the factors that influence all scoring models. These factors matter less than payment history and utilization, but they still contribute to your overall profile.

Check All Three Credit Reports Regularly

Since your credit scores depend entirely on the information in your credit reports, checking those reports makes more sense than obsessing over specific score numbers. You can access your credit reports from all three bureaus for free once per week at AnnualCreditReport.com.

When you review your reports, look for errors, accounts you do not recognize, or negative information that should have aged off your record. Mistakes in your credit reports can drag down your scores across all models, so catching and disputing errors provides benefits regardless of which scoring formula a lender uses.

Understand the Numbers You See

When you check your credit score through any service, pay attention to the fine print that tells you which scoring model and which credit bureau provided the number. This context helps you understand how the score you see relates to what lenders might use.

If you are planning a major credit application like a mortgage or auto loan within the next few months, consider purchasing your scores from the specific models lenders use for that type of borrowing. myFICO.com offers access to dozens of different FICO scores, including the mortgage-specific versions lenders rely on. This investment provides the most accurate picture of how lenders will view your application.

The Bottom Line on Multiple Credit Scores

Having multiple credit scores is not a problem to solve but a reality to understand. The system developed this way because different lenders have different needs, and scoring companies compete to offer the most accurate predictions for each lending situation.

Rather than worrying about which specific number represents your true creditworthiness, focus on the behaviors that build strong credit across all models. Pay your bills on time, keep your balances low, maintain old accounts, and apply for new credit only when you truly need it. These habits will serve you well no matter which scoring formula a lender applies to your file.

When the time comes to apply for a major loan, you can investigate which scores your lender will use and plan accordingly. Until then, treat any credit score you see as a helpful indicator of your progress rather than a definitive judgment on your financial life.

Leave a Reply