You have found the perfect car. It shines under the dealership lights, smells new, and feels like freedom on four wheels. Then you sit down with the finance manager, and the numbers start flying. Monthly payment, interest rate, loan term. Suddenly that beautiful car feels like a financial trap waiting to spring.

Understanding what you can actually afford before you step foot on a dealership lot is the difference between a smart purchase and a years-long regret. And because your credit score determines your interest rate, it also determines how much car you can truly afford.

The 20/4/10 Rule

Before diving into credit tiers, start with the industry standard for car affordability: the 20/4/10 rule. This framework provides a reality check regardless of your credit situation.

20% down payment. Put at least 20% down on your vehicle. This prevents you from owing more than the car is worth the moment you drive off the lot, a situation called being “upside down” on your loan.

4-year maximum loan term. Limit your loan to four years or less. Longer terms mean paying more interest and being stuck with a car you may want to trade long before the loan ends.

10% of monthly income. Keep your total monthly car expenses, including payment, insurance, and estimated maintenance, under 10% of your gross monthly income.

For someone earning $60,000 annually ($5,000 monthly), this means total car costs should stay under $500 per month. With 20% down on a $25,000 car ($5,000), you would finance $20,000. A 48-month loan at 6% yields a $470 payment, leaving room for insurance.

How Credit Tiers Affect Your Payment

Your credit score determines your interest rate, and your interest rate determines how much car you can afford for the same monthly payment. The difference between tiers is dramatic.

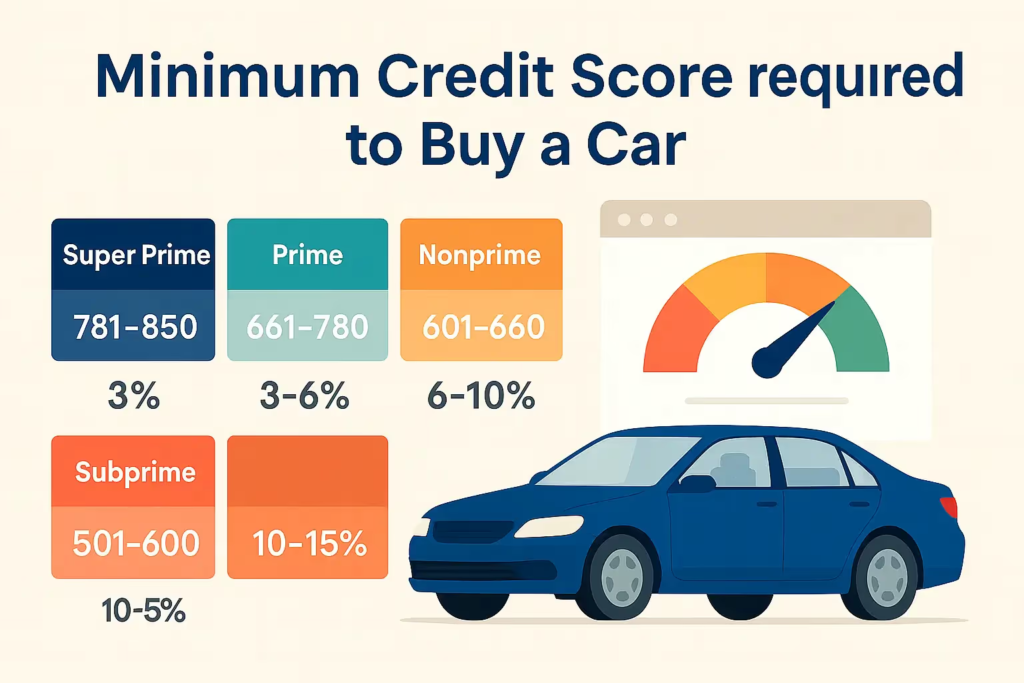

Based on recent data from Experian and Edmunds, here are average auto loan rates for new cars by credit tier :

| Credit Tier | Score Range | Average APR (New Car) |

| Super Prime | 781-850 | 5.25% – 6.25% |

| Prime | 661-780 | 6.75% – 8.50% |

| Non-Prime | 601-660 | 9.50% – 13.50% |

| Subprime | 501-600 | 14% – 18% |

| Deep Subprime | 300-500 | 18% – 24%+ |

Used car rates are typically 1% to 3% higher across all tiers.

Now let’s see what these rates mean for your buying power.

Scenario: The $400 Monthly Payment

Assume you can afford $400 per month for a car payment, and you have 20% down for a 48-month loan. Here is how much car you can buy at each credit tier.

Super Prime (6% APR): With $400 monthly, you can finance approximately $17,000. Add your 20% down, and your total car budget is about $21,250.

Prime (8% APR): Same $400 monthly finances about $16,400. Total car budget: $20,500.

Non-Prime (12% APR): $400 monthly finances about $15,200. Total car budget: $19,000.

Subprime (16% APR): $400 monthly finances about $14,000. Total car budget: $17,500.

Deep Subprime (22% APR): $400 monthly finances about $11,800. Total car budget: $14,750.

The super prime borrower can afford a car costing nearly $6,500 more than the deep subprime borrower, for the exact same monthly payment. That is the real cost of a low credit score.

Beyond the Payment: Total Interest Costs

The monthly payment tells only part of the story. Total interest over the life of the loan reveals the full impact.

For that same $20,000, 48-month loan:

- At 6%: Total interest $2,550, total repaid $22,550

- At 12%: Total interest $5,300, total repaid $25,300

- At 18%: Total interest $8,200, total repaid $28,200

The deep subprime borrower pays over $5,600 more in interest than the super prime borrower, for the exact same car.

Realistic Budgets by Credit Tier

Now let’s build realistic car budgets for each credit tier based on typical household income.

Super Prime (781-850)

If you have excellent credit, you qualify for the lowest rates and best terms. Your focus should be on maximizing value without overspending.

For a household earning $75,000, the 20/4/10 rule suggests total car costs under $625 monthly. With excellent rates, you can afford a $30,000 to $35,000 vehicle with 20% down and a 48-month loan.

You have the flexibility to choose between new and used, and you may qualify for 0% APR manufacturer financing on select new models, which effectively eliminates interest entirely.

Prime (661-780)

Prime borrowers still qualify for competitive rates, though slightly higher than the top tier. Your buying power remains strong.

For a $60,000 household, target $500 monthly total car costs. With 8% APR, you can afford a $22,000 to $25,000 vehicle with 20% down. New cars are accessible, but you may find better value in certified pre-owned vehicles that offer lower prices and still include warranties.

Non-Prime (601-660)

This is the largest segment of car buyers, often called “near-prime.” Your rates are noticeably higher, which means you must adjust your expectations.

For a $50,000 household, target $415 monthly total car costs. With 12% APR, you can afford approximately $16,000 to $18,000 with 20% down. This budget points you toward reliable used cars rather than new ones.

Focus on vehicles known for longevity, like Honda Civic, Toyota Corolla, or Mazda3, that will still be running after your loan is paid off.

Subprime (501-600)

Subprime borrowers face significant rate penalties. Your focus must shift from “what car do I want” to “what reliable transportation can I afford.”

For a $45,000 household, target $375 monthly total car costs. With 16% APR, you can afford approximately $12,000 to $14,000 with 20% down. This puts you in the used car market, likely vehicles 5-8 years old with 60,000 to 100,000 miles.

Consider getting a pre-purchase inspection from an independent mechanic before buying. The $100 inspection fee could save you thousands in repairs.

Deep Subprime (300-500)

If you are in deep subprime territory, your focus must be on survival, not style. Your rates will be extremely high, and many traditional lenders may not approve you at all.

For a $40,000 household, target $330 monthly total car costs. With 20% APR, you can afford approximately $9,000 to $11,000 with 20% down. You are looking at older vehicles, 8-12 years old, with higher mileage.

Consider credit union financing before visiting dealerships. Credit unions often offer better rates to subprime borrowers than buy-here-pay-here lots, which can charge 25% or more and may not even report payments to credit bureaus.

Hidden Costs That Affect Affordability

The monthly payment is only part of your true car cost. Insurance, fuel, maintenance, and registration add significant expenses that vary by vehicle and location.

Insurance costs more for luxury brands, sports cars, and newer vehicles. A 25-year-old with a subprime score might pay $200 monthly just to insure a Honda Civic. Always get insurance quotes before buying.

Fuel costs vary dramatically. A truck costing $400 monthly might require $300 in fuel, while a hybrid with the same payment might need only $100.

Maintenance increases with vehicle age. That $10,000 used car may need $1,000 in repairs within the first year. Factor this into your budget.

Improving Your Position Before Buying

If your credit tier puts your target car out of reach, consider delaying your purchase to improve your position.

Spend six months paying down debt and making all payments on time. Even a 30-point score increase could move you from subprime to non-prime, saving thousands in interest.

Save a larger down payment. Every extra $1,000 down reduces your loan amount and may qualify you for better rates.

Consider a less expensive vehicle. A $15,000 car with a 48-month loan at 12% costs $395 monthly. A $20,000 car at the same rate costs $527 monthly. That $132 difference could strain your budget.

The Bottom Line

Car loan affordability is not about what the dealer says you can afford. It is about what fits your budget while accounting for your credit tier’s impact on interest rates.

Run the numbers before you shop. Know your credit score, know your monthly budget, and know what that translates to in vehicle price. Walk into the dealership with those numbers written down and refuse to exceed them.

The right car at the wrong price is the wrong car. Your credit tier determines your rates, but your discipline determines whether those rates lead to financial freedom or financial stress.

Leave a Reply