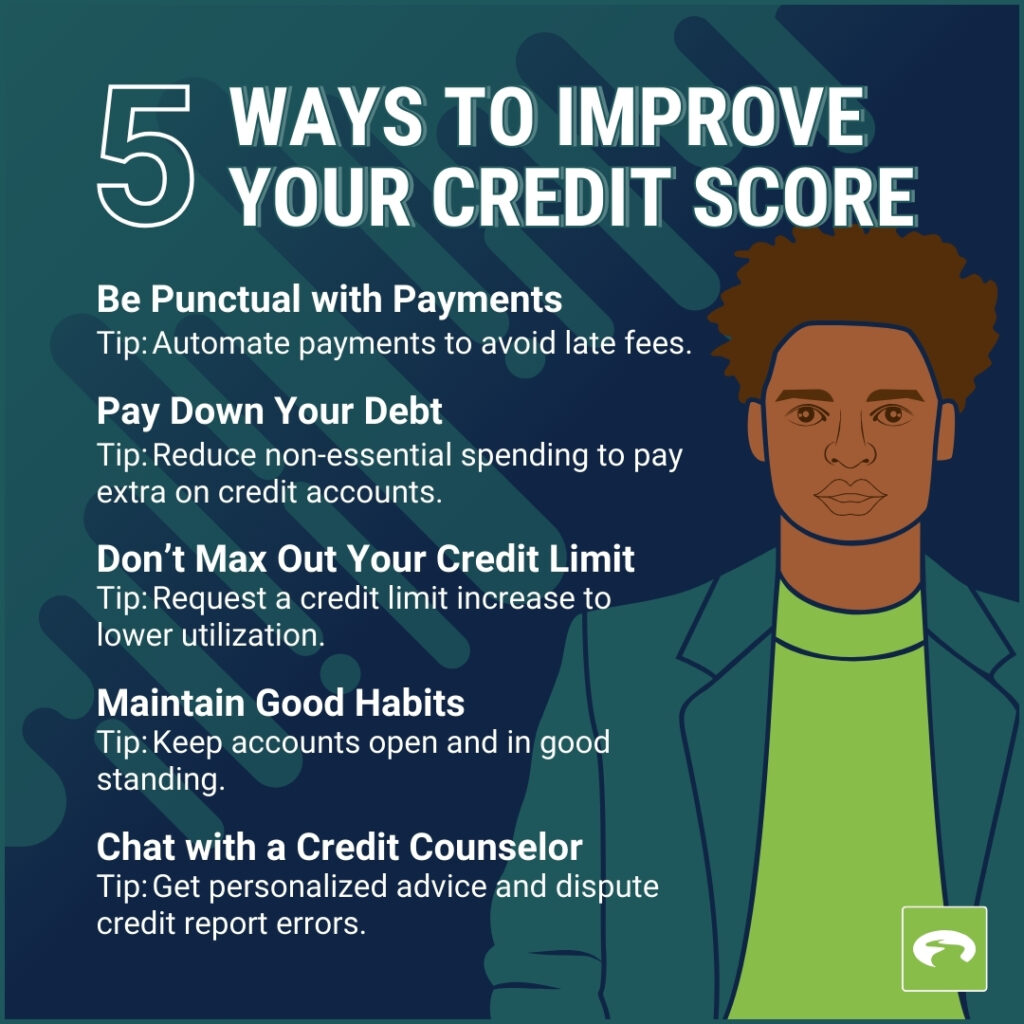

Crossing the 600 threshold feels like climbing out of a deep hole. You have made progress, but you are not where you need to be. Maybe you are stuck at 620, or 640, watching your score move in frustratingly small increments. The difference between a 620 score and a 720 score is not just bragging rights; it is lower interest rates, better credit card offers, and thousands of dollars saved over your lifetime.

The good news is that moving from the 600s into the 700s follows a predictable path. With a systematic month-by-month approach, you can accelerate your progress and reach your goals faster than you might think.

Month 1: The Foundation Audit

Your first month is about diagnosis, not action. You cannot fix what you do not understand.

Start by pulling your credit reports from all three bureaus at AnnualCreditReport.com. You are entitled to free weekly access, so take advantage. Review every single line item. Look for accounts you do not recognize, late payments that should not be there, balances that seem wrong, and collection accounts that may have aged past the seven-year reporting period.

Make a list of any errors you find. For each error, prepare a dispute letter explaining why the information is incorrect and include any supporting documentation you have. The credit bureaus have 30 days to investigate, and if they cannot verify the information, they must remove it.

Check your credit utilization across all cards. Calculate your total balances divided by your total credit limits. If you are above 30%, make a note of which cards are driving that high utilization. These will be your priority targets.

Finally, confirm that you have no missed payments in the last six months. If you do, your immediate priority is establishing a perfect payment streak going forward.

Month 2: Attack Utilization and Errors

With your audit complete, now you execute.

If you found any errors in your credit reports, file those disputes immediately. Send them by certified mail with return receipt requested so you have proof of delivery. The removal of even one incorrect negative item can boost your score by 20 to 50 points or more.

Now focus on utilization. If you have high credit card balances, throw every available dollar at the card with the highest utilization relative to its limit. Scoring models penalize you for maxed-out cards, even if your overall utilization looks okay. Bringing one card from 90% down to 50% can yield faster results than spreading payments across multiple cards.

If you cannot pay down balances significantly this month, consider requesting credit limit increases on cards with perfect payment history. Higher limits instantly lower your utilization without requiring you to pay more. Before requesting, confirm with your issuer that they will use a soft pull rather than a hard inquiry.

Set up automatic payments for at least the minimum amount due on every card. This eliminates any chance of accidental late payments going forward.

Month 3: The Authorized User Strategy

If your credit file is thin or lacks positive history, month three is the time to explore authorized user status.

Ask a trusted family member or close friend with excellent credit if they would add you as an authorized user on one of their oldest, best-managed credit cards. You do not need to use the card or even possess it. The account’s positive history may appear on your credit report as if it were your own.

The ideal account for this strategy has three key features: a long history, perfect payment record, and low utilization relative to its limit. If the primary cardholder manages credit responsibly, this single move can add years of positive history to your file within 30 to 60 days.

Do not pay strangers for this service. Buying tradelines carries significant risks, including fraud accusations and identity theft exposure. Stick to genuine relationships.

Month 4: The AZEO Implementation

With disputes filed and utilization reduced, month four is about precision optimization.

Implement the AZEO method: All Zero Except One. A few days before your statement closing dates, pay down every credit card to a $0 balance except for one. On that remaining card, leave a small balance between 1% and 9% of that card’s limit.

This strategy avoids the “all zero penalty” where scoring models ding you for having no active revolving credit, while still presenting extremely low utilization across your entire portfolio. The effect on your score can be immediate once the new balances are reported.

If you are planning a major credit application like a mortgage or auto loan within the next few months, maintain AZEO consistently during this period. For newer scoring models like FICO 10T that use trended data, consistent low utilization matters more than a one-time optimization.

Month 5: Strategic New Credit

If your credit file has fewer than three open accounts, month five is the time to consider adding a new account.

For those still in the rebuilding phase, a secured card from a reputable issuer like Discover or Capital One provides a reliable path. These cards require a refundable deposit but report to all three bureaus and often graduate to unsecured status after six to twelve months.

If your score has climbed into the mid-600s, you may qualify for a basic unsecured card like the Capital One Platinum or a student card if you are enrolled in school. Compare pre-approval offers online before applying to avoid unnecessary hard inquiries.

Space this application at least six months from any previous applications to minimize the impact of hard inquiries on your score.

Month 6: Review and Adjust

Six months in, it is time to measure progress and adjust your strategy.

Pull your credit reports again and compare them to your starting point. Have your disputes been resolved? Did any negative items fall off? Has your utilization improved? How much has your score moved?

If your score has not improved as much as you hoped, identify the remaining obstacles. Are there negative items you missed? Is your utilization still higher than it should be? Do you need more time to build positive history?

Continue the habits that work: perfect payments, low utilization, regular monitoring. Credit building is a marathon, not a sprint, but with consistent effort, the gains will come.

Months 7-12: Maintenance and Growth

For the remainder of your first year, focus on maintaining momentum.

Request credit limit increases every six months on cards with perfect payment history. More available credit keeps your utilization low even as your spending grows.

Consider adding a second card if your file remains thin. Aim for cards that offer rewards matching your spending patterns, but only if you can manage them responsibly.

Monitor your credit score monthly through free services like Credit Karma or your card issuer’s app. Celebrate small wins and investigate any unexpected drops immediately.

The Road to 700 and Beyond

With consistent effort over 12 to 18 months, moving from the low 600s to the mid-700s is entirely achievable. The key is understanding that different factors move at different speeds.

Payment history builds slowly over time, with each on-time payment adding to your positive record. Utilization responds immediately, making it your fastest lever for improvement. Negative items fade as they age, with the most recent two years carrying the heaviest weight.

By month 12, you should have a thick file with at least three active accounts, all reporting perfect payment history. Your utilization should consistently stay below 10%, and any errors or outdated negatives should be long gone. At this point, you are no longer rebuilding; you are optimizing.

The journey from 600 to 700 is not mysterious. It follows a roadmap that thousands have successfully navigated before you. Follow these steps month by month, and your score will reflect your effort.

Leave a Reply