The question echoes in the mind of every aspiring homeowner: “What credit score do I actually need?” You’ve checked your score online, seen a number, and have absolutely no idea if it’s enough. The short answer is that it depends entirely on which loan program you choose, how much you can put down, and who your lender is.

Here is the truth that might surprise you: you can technically buy a house with a credit score as low as 500. But you can also be denied with a score of 680. The number alone doesn’t tell the whole story.

Let’s run the mortgage simulation across every major loan type so you can see exactly where you stand in 2026.

The Major Shift: Conventional Loans Just Changed Everything

If you are aiming for a conventional loan, the landscape shifted dramatically in late 2025. Fannie Mae, one of the two government-sponsored enterprises that back most conventional mortgages, eliminated its minimum credit score requirement entirely on November 15, 2025.

This does not mean you can buy a house with a 300 credit score. It means that instead of a hard cutoff, lenders now evaluate your entire financial picture: your cash reserves, your debt levels, the property characteristics, and your overall credit history. The old 620 floor for conventional loans is now more of a guideline than a rule, though most lenders still use it as a practical benchmark.

For borrowers with scores between 620 and 639 on a $400,000 loan, the estimated APR in late 2025 was approximately 7.768%, with a monthly payment around $2,860 and total lifetime interest of approximately $728,600. That same loan with a score of 760 or above dropped to 7.037% APR, $2,324 monthly, and $535,640 total interest—a savings of nearly $200,000 over 30 years.

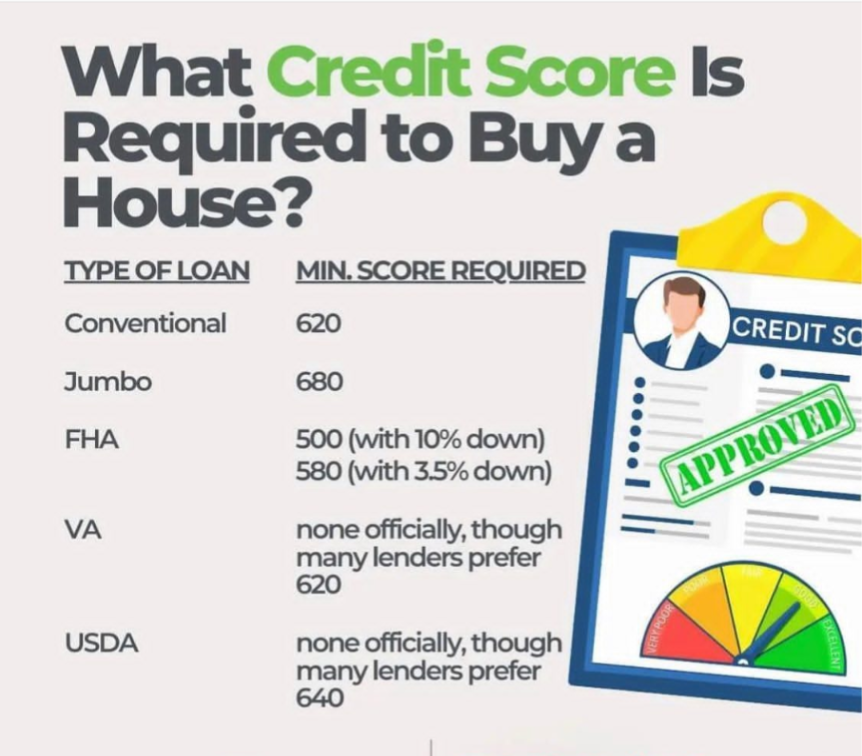

FHA Loans: The Low-Score Champion

If your credit needs work, FHA loans remain the most accessible path to homeownership. The Federal Housing Administration sets the official floor at 500, though the terms change dramatically depending on where you land.

With a credit score of 580 or higher, you qualify for the FHA’s flagship 3.5% down payment program. This is the sweet spot for first-time buyers and those rebuilding credit.

With a credit score between 500 and 579, you can still qualify, but you will need to put 10% down. This higher down payment partially offsets the lender’s risk.

Below 500, standard FHA channels generally will not approve you.

Here is the catch that trips up many applicants: lenders can and do set their own requirements above the FHA’s minimums. These are called “overlays.” A lender might require 620 even though FHA allows 580. Shopping multiple lenders is not optional; it is strategy.

FHA loans also come with mortgage insurance premiums (MIP) that add to your costs. The upfront premium is 1.75% of your loan amount, typically rolled into the loan. The monthly premium runs 0.45% to 1.05% annually, and if you put down less than 10%, that monthly MIP lasts for the entire 30-year loan term unless you refinance.

VA Loans: The Veteran’s Advantage

For eligible veterans, active-duty service members, and qualifying surviving spouses, VA loans offer terms that no other program can match. The VA itself sets no minimum credit score requirement.

However, private lenders who issue the loans do set their own requirements. Most VA lenders look for a minimum median FICO score of 620, though some will go as low as 580 with compensating factors like stable employment or significant cash reserves.

The benefits are extraordinary: zero down payment, no private mortgage insurance, competitive interest rates typically below conventional loans, and flexible credit guidelines. The tradeoff is a VA funding fee between 1.25% and 3.3% of the loan amount, though this can be financed into the loan.

Half of all veterans either do not know the credit requirements for VA loans or believe they need much higher scores than are actually necessary. If you have served, this is likely your best option.

USDA Loans: Rural and Suburban Opportunity

USDA loans target low-to-moderate income buyers in qualifying rural and suburban areas. The program offers 100% financing, meaning no down payment required.

The USDA’s automated underwriting system and most lenders require a score of 640 to streamline approval. Some lenders may negotiate with slightly lower scores, but 640 is the practical cutoff.

Income limits apply based on your location and household size. In Florida, for example, households with 1-4 members cannot exceed roughly $119,850 gross annual income, though this varies by county. The property itself must be in a USDA-eligible area, which covers about 97% of U.S. landmass but excludes most major metropolitan centers.

Jumbo Loans: High-Balance Requirements

If you need a loan above the conforming limit of $832,750 (or higher in expensive markets), you enter jumbo loan territory. These loans exceed Fannie Mae and Freddie Mac’s purchase limits, meaning lenders hold more risk and therefore set stricter requirements.

Most jumbo lenders require a credit score of 700 or higher, with some accepting 680 if you have substantial cash reserves and a larger down payment, typically 10% to 20%.

The Real Numbers: What Different Scores Actually Get You

Let’s simulate a $400,000 purchase with 5% down across different credit tiers, based on FICO’s mortgage calculator data from October 2025 :

| Credit Score Range | Estimated APR | Monthly Payment | Total Interest Over 30 Years |

| 760+ | 7.037% | $2,324 | $535,640 |

| 700-759 | 7.193% | $2,383 | $556,920 |

| 680-699 | 7.422% | $2,460 | $588,240 |

| 660-679 | 7.684% | $2,545 | $622,440 |

| 640-659 | 8.048% | $2,655 | $671,040 |

| 620-639 | 8.352% | $2,742 | $728,600 |

The difference between the top and bottom tier is approximately $536 per month and $192,960 over the life of the loan.

Private mortgage insurance adds another layer. With 5% down, a borrower with a 760+ score pays roughly 0.38% annually in PMI. A borrower with a 680-699 score pays approximately 0.96% annually. On a $380,000 loan, that is an extra $2,200 per year in PMI costs for the lower-score borrower.

Beyond the Score: What Lenders Actually Evaluate

Your credit score opens the door, but it does not determine everything. Lenders scrutinize multiple factors in what they call your “full financial picture”.

Debt-to-income ratio (DTI) measures your monthly debt obligations divided by your gross monthly income. Most lenders prefer 43% or lower, though FHA allows up to 50% with compensating factors, and some conventional programs stretch to 50% as well.

Down payment matters enormously. A larger down payment offsets lower credit scores. The median down payment for first-time buyers is 10%, though conventional loans allow as little as 3% and FHA allows 3.5%.

Cash reserves show you can handle unexpected expenses. Lenders like to see several months of mortgage payments in reserve after closing.

Employment history should show stability, typically two years in the same line of work.

The Bottom Line

The credit score you need to buy a house ranges from 500 for FHA with 10% down to 620 for most conventional and VA loans to 640 for streamlined USDA approval to 700+ for jumbo financing.

But the number on your credit report is only one piece of a larger puzzle. In 2026, lenders have more tools than ever to evaluate your true financial health, including trended data that looks at your credit behavior over time and alternative data like rent and utility payments.

If your score is lower than you would like, do not assume homeownership is out of reach. Run the numbers for each loan type, talk to multiple lenders, and understand that even a 20 to 40 point improvement can save you tens of thousands of dollars over the life of your loan. The path to your front door starts with knowing exactly where you stand and which program fits your profile.

Leave a Reply