You pay your credit card bills on time every month. You never carry a balance. Your credit score should be perfect, right? Then why did it just drop 15 points for no apparent reason? If this scenario sounds familiar, you may have stumbled into one of credit scoring’s most frustrating paradoxes: the “all zero penalty.” Enter the AZEO method, an advanced strategy that credit enthusiasts swear can squeeze every last point out of your score exactly when you need it most.

What Is the AZEO Method?

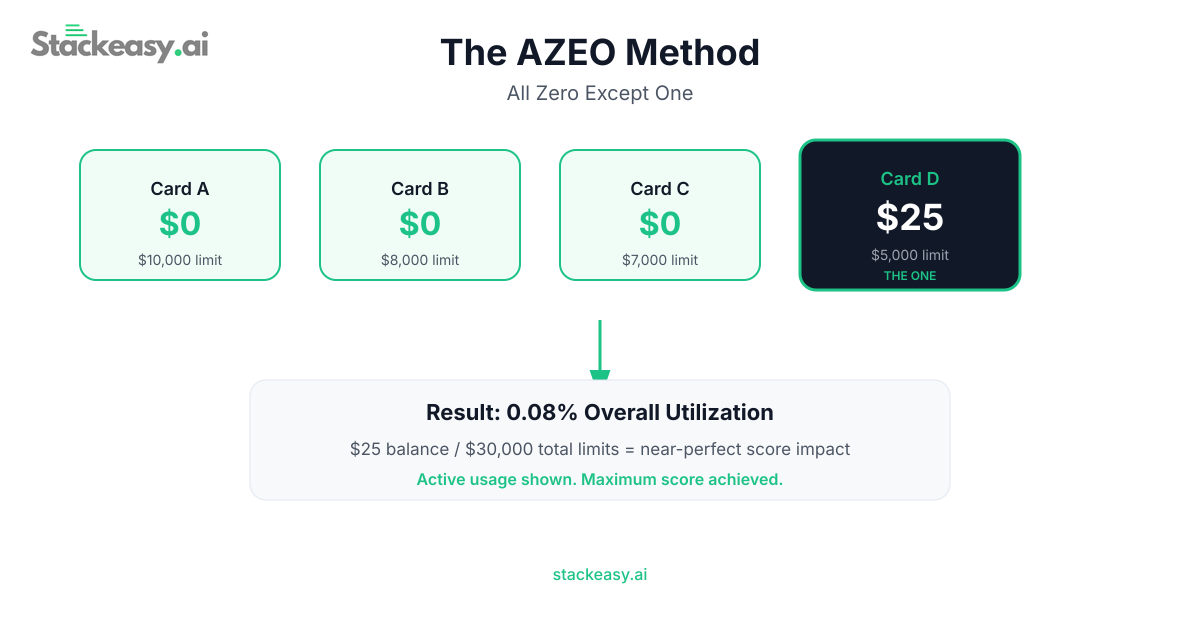

AZEO stands for “All Zero Except One.” The concept is deceptively simple: before your credit card statement closing dates, you pay down every single one of your credit cards to a $0 balance—except for one. On that one remaining card, you leave a small balance, ideally between 1% and 9% of that card’s credit limit.

This strategy targets your credit utilization ratio, which accounts for 30% of your FICO score and is the second-most important factor after payment history. Credit utilization measures how much of your available credit you are using at any given time. When you optimize this ratio through AZEO, you present the most attractive possible profile to scoring algorithms.

Why the “All Zero” Penalty Exists

The logic behind AZEO hinges on understanding why scoring models penalize zero balances across all cards. You might assume that showing $0 in credit card debt would be ideal. But most FICO scoring models slightly ding consumers who have all revolving accounts reporting a $0 balance.

Why? The algorithms interpret total inactivity as a lack of recent data on how you manage repayment. They prefer seeing active, responsible usage over no usage at all. A card reporting a zero balance looks like it isn’t being used, which provides no information about your repayment behavior.

One consumer documented this phenomenon firsthand, observing that 0% utilization caused their FICO score to fall by 15 to 20 points, while their VantageScore remained stable. This difference highlights how various scoring models treat utilization differently, with FICO being particularly sensitive to the all-zero scenario.

How AZEO Optimizes Both Utilization Metrics

To understand why AZEO is so effective, you need to know how credit scoring models evaluate utilization on two levels :

Overall utilization looks at your total balances across all cards divided by your total credit limits. This gives lenders a broad view of how much of your available credit you are using.

Per-card utilization examines each individual card’s balance relative to its limit. Scoring models penalize you for having any single card maxed out, even if your overall utilization looks healthy.

AZEO satisfies both criteria perfectly. By bringing every card except one to zero, your per-card utilization on those accounts drops to 0%, which is excellent. By leaving a small balance on that final card, you keep your overall utilization in the optimal 1% to 9% range, avoiding the all-zero penalty while still showcasing incredibly low credit usage.

The Step-by-Step AZEO Implementation Guide

Ready to put AZEO into practice? Follow these steps in the month leading up to a major credit application :

Step 1: Identify your statement closing dates. Log into each of your credit card accounts and find the statement closing date, not the payment due date. This is the date your issuer reports your balance to the credit bureaus. Add these dates to your calendar with reminders to pay a few days beforehand.

Step 2: Choose your “except one” card strategically. Select the card where you will leave a small balance. Experts recommend using the card with the highest credit limit, as this allows you to report a higher dollar amount while still staying under 9% utilization. Avoid using charge cards like the American Express Gold or Platinum for this purpose, as they operate under different rules.

Step 3: Pay down all other cards to zero. A few days before each card’s statement closing date, make a payment bringing the balance to $0. Confirm that the payment has posted before the closing date arrives.

Step 4: Leave 1% to 9% on your chosen card. On your selected card, allow a small balance to post. For a card with a $5,000 limit, this means leaving between $50 and $450 to be reported. Some experts suggest an even narrower range of 1% to 6% for optimal results.

Step 5: After statements close, pay that small balance. Once your statement generates and the low balance has been reported, you can pay off that remaining amount immediately to avoid any interest charges.

What AZEO Does Not Do

It is crucial to understand the limitations of this strategy. AZEO is a tactical tool for short-term score optimization, not a long-term credit management philosophy. For your monthly routine, simply paying your full statement balance by the due date is perfectly sufficient to maintain good credit.

The reason AZEO is unnecessary for daily life comes down to a fundamental feature of current FICO models: utilization has no memory. Your score only cares about the last reported utilization from each card. A month of high utilization is forgotten as soon as the next month reports low utilization. This means you only need to implement AZEO in the one to two billing cycles before you apply for a mortgage, auto loan, or other major credit.

One Reddit user who tried the AZEO method for six months found that between having one-fifth versus three-fifths of their cards reporting balances, they saw only a two to three point difference. They ultimately decided the micromanagement was not worth the minimal gain for everyday credit health.

Real-World Results and Considerations

The effectiveness of AZEO depends heavily on your starting point and the scoring model being used. For someone with otherwise excellent credit but slightly elevated utilization, AZEO can provide the final polish that pushes their score into the highest tier. For someone with thin credit or recent negative items, the impact will be less dramatic.

Different scoring models also respond differently. One observer noted that 0% utilization caused their FICO score to drop 15-20 points while their VantageScore remained stable, suggesting that VantageScore users may not need to worry as much about the all-zero penalty.

The method also works best with traditional revolving credit cards. Store cards and charge cards may report differently, and some credit builder products have their own unique reporting patterns.

Common Mistakes to Avoid

When implementing AZEO, watch out for these pitfalls:

Paying on the due date instead of the closing date. Your payment due date comes after your statement closes. Paying then means the high balance has already been reported.

Leaving too large a balance. Keeping your “except one” card under 10% is good, but under 5% or even 1-2% may be even better for maximizing every possible point.

Forgetting that all cards at $0 triggers the penalty. This is the entire reason AZEO exists. Do not accidentally pay every card to zero.

Implementing AZEO year-round when it isn’t needed. Constant micromanagement creates unnecessary stress and makes minimal difference over simply paying your bills on time.

The Bottom Line

Does the AZEO method really work? Yes, for its intended purpose. When you need to present the most optimized credit profile possible before a major loan application, AZEO gives you direct control over the 30% of your score tied to credit utilization. It avoids the all-zero penalty while showcasing incredibly low balances across your entire credit portfolio.

However, AZEO is not a magic bullet for fundamentally poor credit. The foundation of an excellent score will always be long-term, on-time payments, which account for 35% of your FICO score, and a long credit history, which accounts for another 15%. Think of AZEO as the cherry on top of a well-built credit sundae—delightful when you need to impress, but meaningless without the substance underneath.

For everyday life, simply paying your statement balances in full by the due date remains the golden rule. Save the AZEO strategy for the months when you need to put on a perfect show for lenders, and you will have mastered one of the most sophisticated tools in the credit optimization playbook.

Leave a Reply