When bankruptcy becomes a consideration, understanding the difference between secured and unsecured debt determines what you keep, what you lose, and how the entire process unfolds. These two categories operate under completely different rules, and confusing them can lead to costly mistakes at the worst possible time.

The fundamental distinction is simple but powerful: secured debt is tied to specific property, while unsecured debt is not. That difference determines everything about how bankruptcy treats each type of obligation.

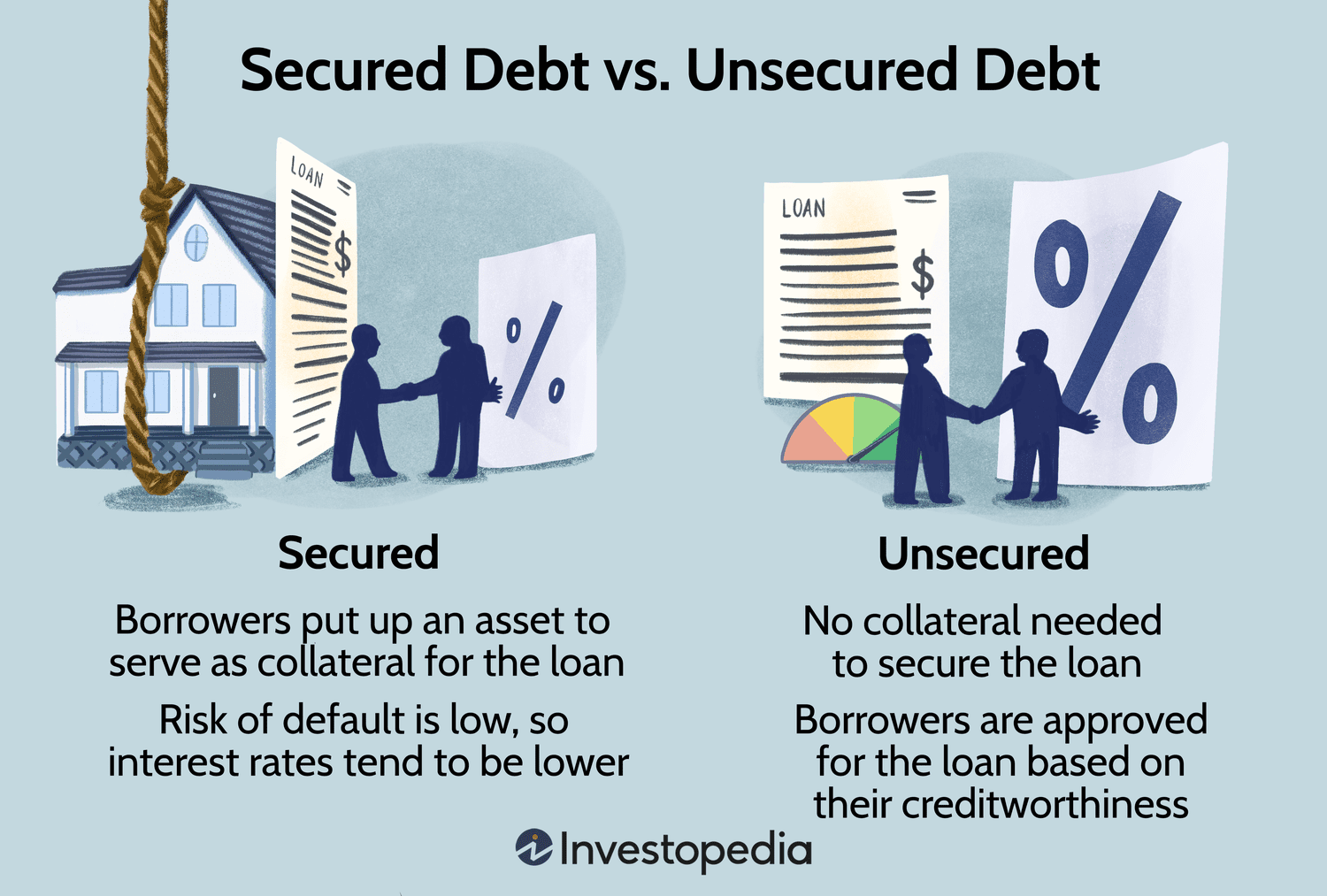

What Makes Debt Secured

Secured debt is backed by collateral. When you borrow money, you pledge an asset that the lender can take if you fail to repay. This connection between the loan and the property defines secured debt.

Mortgages are the most common example. Your home secures the loan, and if you stop paying, the bank can foreclose and take the property. Auto loans work the same way. Your car secures the debt, and the lender can repossess it upon default.

Other forms of secured debt include home equity lines of credit, secured credit cards where your deposit backs the line, and loans secured by personal property like boats, RVs, or expensive jewelry. In each case, the lender has a legal right to specific assets.

The key feature of secured debt is priority. In bankruptcy, secured creditors have first claim to their collateral. They get the property or its value before any unsecured creditors receive anything.

What Makes Debt Unsecured

Unsecured debt has no collateral backing it. The lender lent you money based on your promise to repay, with no specific asset pledged as security. If you default, the lender cannot simply take your property. They must sue you, obtain a judgment, and then use legal processes to enforce collection.

Credit cards represent the largest category of unsecured debt. Store cards, personal loans from online lenders, medical bills, and most student loans also fall into this category. These lenders took a risk when they lent you money, and in bankruptcy, they accept that they may recover only pennies on the dollar.

Unsecured debt divides further into priority and non-priority categories. Priority unsecured debts include most taxes, child support, and alimony. These get paid before other unsecured debts if any funds remain. Non-priority unsecured debts, including credit cards and medical bills, are last in line.

How Bankruptcy Treats Secured Debt

In bankruptcy, you have options with secured debt. You can keep the property and continue paying, or you can surrender it and walk away.

If you want to keep your home or car, Chapter 7 bankruptcy requires you to continue making regular payments and stay current on the debt. The bankruptcy discharge eliminates your personal liability, meaning the lender cannot sue you for any deficiency if you later default, but they can still repossess the property if you stop paying.

If you are behind on payments, Chapter 7 offers limited help. The lender can still foreclose or repossess once the automatic stay lifts unless you catch up quickly.

Chapter 13 bankruptcy provides more powerful tools for secured debt. You can catch up missed payments through a court-approved repayment plan over three to five years. As long as you make plan payments, foreclosure and repossession cannot proceed.

Chapter 13 also offers the “cramdown” option for certain secured debts. If you owe more on a vehicle than it is worth, you may be able to reduce the loan balance to the car’s actual value and pay that amount through your plan. This provision does not apply to mortgages on primary residences.

How Bankruptcy Treats Unsecured Debt

Unsecured debt is where bankruptcy provides the most relief. In Chapter 7 bankruptcy, most unsecured debts are completely discharged. You walk away owing nothing on credit cards, medical bills, and personal loans.

There are exceptions. Student loans are notoriously difficult to discharge, requiring proof of undue hardship that few borrowers meet. Recent tax debts, child support, alimony, and debts from fraud or intentional wrongdoing survive bankruptcy.

In Chapter 13, unsecured creditors receive only what you can afford to pay after secured debts and priority claims are handled. If your disposable income is limited, unsecured creditors may receive pennies on the dollar, and any remaining balance is discharged after you complete your plan.

The “means test” determines whether you qualify for Chapter 7 or must use Chapter 13. If your income exceeds your state median and you have enough disposable income to pay some unsecured debt, you may be forced into Chapter 13 where creditors receive at least some payment.

The Automatic Stay: Immediate Protection

Whether your debt is secured or unsecured, filing bankruptcy triggers the automatic stay. This court order stops all collection activity immediately.

Foreclosure proceedings halt. Repossession attempts stop. Wage garnishments end. Collection calls cease. The automatic stay gives you breathing room to sort out your finances without constant pressure.

For secured debts, the stay is temporary. Lenders can ask the bankruptcy court for permission to proceed with foreclosure or repossession, especially if you are not making payments. But the stay at least buys time to decide whether you want to keep the property.

For unsecured debts, the stay lasts throughout the case and becomes permanent when you receive your discharge. Creditors can never collect on discharged debts again.

What Happens to Your Property

Secured debt determines whether you keep specific assets. If you want to keep your home, you must continue paying the mortgage. If you want to keep your car, you must continue paying the auto loan.

Unsecured debt does not threaten specific property. No creditor can take your television because you have credit card debt. However, Chapter 7 bankruptcy includes a different risk: the trustee can sell non-exempt assets to pay unsecured creditors.

Every state has exemption laws protecting certain property. Homestead exemptions protect home equity up to certain limits. Vehicle exemptions protect your car up to a value threshold. Personal property exemptions cover household goods, clothing, and tools of your trade.

If your assets exceed available exemptions, the trustee can sell them and distribute proceeds to unsecured creditors. This risk is why Chapter 13 may be preferable for those with significant non-exempt assets, as it allows you to keep property while paying its value through your plan.

Real-World Examples

Consider a borrower with $30,000 in credit card debt, a $200,000 mortgage on a home worth $220,000, and a car loan with $15,000 remaining on a vehicle worth $12,000.

The credit card debt is unsecured. In Chapter 7, it is entirely dischargeable. The borrower keeps the home by continuing mortgage payments and keeps the car by continuing loan payments.

The car loan presents a problem because the borrower owes more than the car is worth. In Chapter 13, the borrower might cram down the loan to $12,000, the car’s actual value, and pay that amount through the plan while discharging the remaining $3,000.

Another borrower has $50,000 in credit card debt and $100,000 in home equity with a homestead exemption of $60,000. The $40,000 in unprotected equity could be seized by the Chapter 7 trustee and sold to pay unsecured creditors. This borrower might choose Chapter 13 to keep the home while paying the equity value through the plan.

Making the Right Choice

Understanding secured versus unsecured debt guides your bankruptcy decision. If most of your debt is unsecured and you have few assets, Chapter 7 offers a quick fresh start. If you have significant secured debt you want to keep or non-exempt assets to protect, Chapter 13 provides more tools.

Consulting with a bankruptcy attorney is essential. The interaction between secured and unsecured debt, exemptions, and your specific situation requires professional analysis. Most offer free initial consultations where they can explain which chapter fits your circumstances.

The Bottom Line

Secured debt ties loans to property. Mortgages, auto loans, and secured credit cards fall here. Unsecured debt has no collateral. Credit cards, medical bills, and personal loans are typical examples.

In bankruptcy, secured creditors can take their collateral if you stop paying. Unsecured creditors generally receive only what remains after secured claims, and most unsecured debt is dischargeable.

Knowing the difference determines what you keep and what you lose. It shapes which bankruptcy chapter you choose and how the process affects your future. Take the time to understand your debts before making decisions that impact your financial life for years to come.

Leave a Reply