You see it on every card comparison website and every issuer’s application page: a little label that says “Credit Score Needed: Fair” or “Good/Excellent.” If you are new to credit or rebuilding from past mistakes, those vague categories can feel like a secret code you are not meant to understand. What does “fair” actually mean in numbers? And how can you know whether you qualify before you apply and risk a hard inquiry?

The truth about credit score requirements for starter cards is more nuanced and more hopeful than the marketing suggests. Understanding what issuers actually look for when you have limited history can save you from unnecessary rejections and point you toward cards that will genuinely approve you.

The Truth About “No Credit” vs. “Bad Credit”

The first distinction you need to understand separates having no credit from having bad credit. Starter cards treat these two situations very differently, and confusing them leads to unnecessary denials.

No credit means exactly what it sounds like: your credit file contains little to no information. You have never had a loan, never carried a credit card, and never appeared in the credit bureaus’ databases except perhaps as an authorized user on someone else’s account. This situation describes most young adults, recent immigrants, and anyone who has simply never borrowed money.

Bad credit means you have credit history, but it contains negative information. Late payments, collections, charge-offs, or high utilization have damaged your score. Lenders see evidence that you have struggled with credit in the past.

Most top starter cards are designed specifically for the “no credit” crowd. Student cards from Discover and Capital One, for example, expect you to have little or no history. They are not looking for excellent scores; they are looking for proof that you are who you say you are and that you have some income to support repayment.

Cards for bad credit, by contrast, often come with higher fees, secured deposits, or more restrictive terms. The distinction matters because applying for a “bad credit” card when you have no credit may land you with unnecessary fees, while applying for a “no credit” card when you have negative history may result in rejection.

What “Fair” and “Limited History” Actually Mean

When you see a card described as requiring “Fair” credit or accepting “Limited History,” the issuer is using shorthand for a range of credit scores and situations.

According to WalletHub’s analysis for February 2026, the Capital One Savor Student Cash Rewards Credit Card, the Discover it Secured Credit Card, and the Petal 2 Visa Credit Card all fall into the “Fair” or “Limited History” categories. But these cards evaluate applicants very differently.

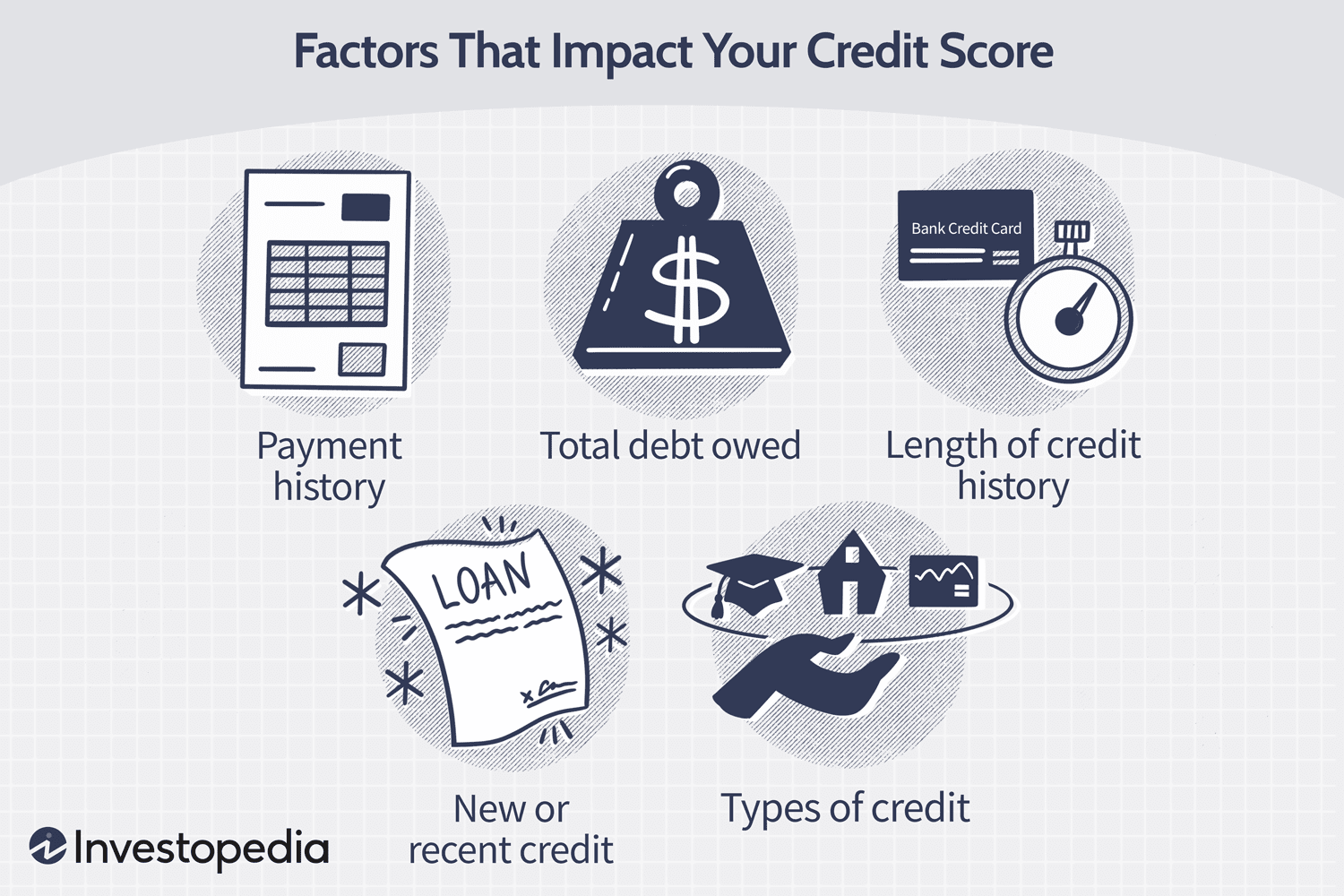

For most lenders, “Fair” credit generally means FICO scores in the 580 to 669 range. However, for starter cards specifically, “Limited History” often means you have fewer than three accounts on your credit report or your oldest account is less than three years old. Some applicants with no score at all still qualify because the issuer uses alternative data.

The Petal 2 Visa, for example, uses a proprietary “Cash Score” that looks at your banking activity and income rather than just your credit history. This innovation has opened doors for thousands of applicants who would be denied under traditional underwriting.

The key insight is that “credit score needed” is not a hard cutoff for most starter cards. Issuers consider your entire financial picture, including income, existing relationships with the bank, and alternative data points that predict your likelihood of repaying.

Top Starter Cards and Their Real Requirements

Let us look at what specific starter cards actually require in practice, based on current 2026 data.

Discover it Secured Credit Card

Discover explicitly states that “no credit score is required to apply” for its secured card. This does not mean everyone is approved, but it means Discover evaluates applicants based on the information they provide rather than rejecting anyone without a pre-existing score.

The card requires a refundable security deposit starting at $200, and Discover automatically reviews accounts for potential graduation to unsecured status starting at seven months. For true beginners with no credit history, this card represents one of the most accessible options available.

Capital One Savor Student Cash Rewards Credit Card

This student card accepts applicants with “fair” or “limited” credit history. For students enrolled in college, Capital One may approve applicants with no credit history at all, provided they can demonstrate sufficient income from part-time jobs, work-study, or family support.

The card offers 3% cash back on dining, entertainment, streaming services, and grocery stores, with a $50 bonus after spending $100 in the first three months. It has no annual fee and reports to all three credit bureaus monthly.

Petal 2 Visa Credit Card

The Petal 2 card represents a new breed of starter cards that use alternative underwriting. According to Chime’s analysis, Petal uses a “Cash Score” that evaluates your banking activity, not just your credit history. This means applicants with no credit score can qualify if they demonstrate responsible banking habits.

The card offers 1% cash back on all purchases, increasing to 1.25% after six months of on-time payments and 1.5% after twelve months. There are no annual, late, or foreign transaction fees, making it one of the most fee-friendly options for beginners.

Capital One Platinum Credit Card

The Capital One Platinum card is designed for those with limited credit history who want a simple, no-frills card to build credit. It has no annual fee and no rewards, focusing purely on providing a path to credit building.

Capital One automatically reviews accounts for potential credit limit increases after as little as six months of responsible use. This feature helps beginners increase their available credit and lower their utilization over time.

Chime Card

The Chime Card offers a unique approach with no credit check required to apply. Instead of a traditional security deposit, money added to your Chime Checking Account becomes your spending limit. This structure prevents overspending while building credit through monthly reporting to all three bureaus.

Chime also offers rent reporting, which can help build credit through on-time rent payments. For those who struggle with traditional credit card structures, this alternative path provides access without risk of debt.

What Issuers Actually Look For

Understanding what issuers want beyond your credit score helps you position yourself for approval even if your numbers are not where you want them.

Income matters enormously. Credit card issuers must verify that you have the means to repay what you borrow. For students and young adults, this can include part-time wages, regular allowances from family, or work-study income. The CARD Act of 2009 requires applicants under twenty-one to demonstrate independent income, so having that documentation ready speeds the process.

Banking relationships help. Applying for a card with a bank where you already have checking or savings accounts improves your odds. The bank can see your deposit history and verify that you manage money responsibly. Discover, Capital One, and Chase all consider existing relationships when evaluating thin-file applicants.

Enrollment status matters for student cards. If you are applying for a student card, you typically need to provide proof of enrollment at an accredited college, university, or community college. Some issuers also accept applicants who have been admitted and plan to enroll within the next few months.

Alternative data can fill gaps. Companies like Petal and Chime have pioneered the use of bank account data, rent payments, and utility bills to evaluate applicants without traditional credit scores. If you have been denied elsewhere, these alternative-path cards may offer approval where traditional issuers will not.

The Difference Between Secured and Unsecured Starter Cards

One of the most important distinctions in starter cards is whether they require a security deposit. Secured cards like Discover it Secured and Capital One Quicksilver Secured require upfront deposits that become your credit limit. Unsecured starter cards like the Petal 2 Visa and Capital One Platinum do not.

Secured cards typically offer easier approval because the deposit protects the issuer against losses. If you have no credit or very damaged credit, a secured card may represent your most reliable path to approval.

Unsecured starter cards offer the advantage of not tying up your cash, but they may have stricter approval criteria. The Petal 2 Visa, for example, requires you to link a bank account and demonstrate responsible banking history.

How to Check Your Odds Without Hurting Your Score

Before applying for any card, you can take steps to understand your approval odds without triggering a hard inquiry that temporarily lowers your score.

Use pre-approval tools. Many issuers offer online pre-approval forms that check your eligibility using only a soft inquiry. Discover, Capital One, and Petal all provide these tools on their websites. Completing a pre-approval form tells you which cards you likely qualify for without any impact on your credit.

Check your credit score for free. Apps like Credit Karma, CreditWise from Capital One, and Discover’s Credit Scorecard provide free access to your credit scores. While these may be VantageScores rather than FICO scores, they give you a general sense of where you stand.

Review your credit reports. AnnualCreditReport.com offers free weekly access to your reports from all three bureaus. Reviewing them helps you spot errors that could drag down your score and identify any negative items that might affect approval.

Know what you bring to the table. Before applying, gather information about your income, housing costs, and existing banking relationships. Having this information ready helps you complete applications accurately and honestly.

Common Myths About Credit Score Requirements

Several persistent myths about credit score requirements keep people from applying for cards they could actually get.

Myth: You need a credit score to get any credit card. False. Many starter cards explicitly accept applicants with no credit history. Student cards, secured cards, and alternative-data cards all provide paths for those without scores.

Myth: Checking your own score lowers it. False. Checking your own credit through free services or annual credit reports uses a soft inquiry that does not affect your score. Only hard inquiries from lenders impact your credit.

Myth: If you are denied once, you cannot get any card. False. Different issuers use different criteria. A denial from Chase does not predict denial from Discover or Capital One. Learning why you were denied helps you address issues and try again with better odds.

Myth: Store cards are easier to get than real credit cards. Not necessarily. Some store cards have easier approval, but they also come with high interest rates and low limits that can hurt your utilization. A secured card from a major issuer often provides better long-term value.

The Bottom Line

When you see “Credit Score Needed” on a starter card, translate it as “Approval Factors Considered” instead. Issuers look at your income, your banking history, your enrollment status, and your overall financial picture alongside whatever credit information exists.

For true beginners with no credit history, student cards and secured cards from major issuers offer the most reliable paths to approval. For those with thin files but responsible banking habits, alternative-data cards like Petal 2 provide unsecured options without deposits.

The most important step is applying strategically rather than randomly. Use pre-approval tools, understand what each card requires, and choose the card that best matches your specific situation. With the right approach, that mysterious “Credit Score Needed” label becomes a guide rather than a barrier.

Leave a Reply