Your credit score is a three-digit number that wields enormous power over your financial life. It influences whether you get approved for a mortgage, what interest rate you pay on a car loan, and even how much you shell out for insurance premiums. Yet for something so important, it remains shrouded in mystery for many Americans. The good news is that the formula behind your credit score is not a secret. By understanding the five factors that go into the calculation, you can take control of your financial reputation and make strategic decisions that move the needle in your favor.

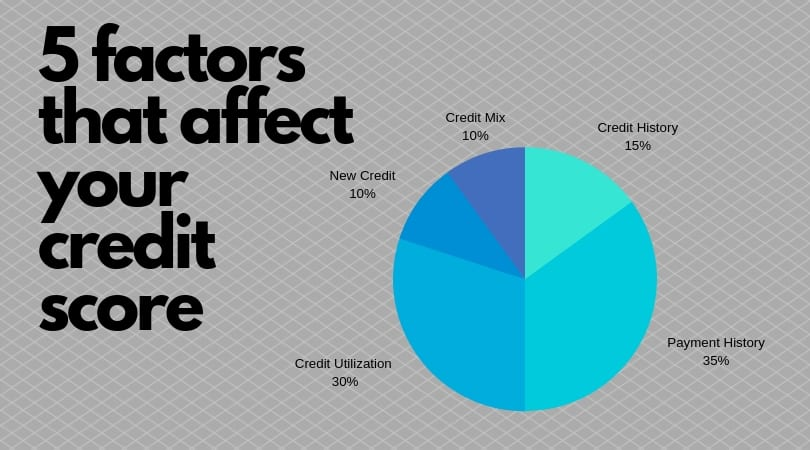

The two major scoring models used by lenders today are FICO and VantageScore. While they have slight differences, both evaluate the same core behaviors. FICO breaks its scoring down into five specific categories with assigned weights, making it the easiest model to understand and the one used by ninety percent of top lenders. VantageScore uses six categories, but the underlying principles remain remarkably similar. Let us explore each factor in detail and reveal which one truly matters most for your financial health.

Payment History: The Undisputed King of Credit Scoring

If you take away only one lesson from understanding credit scores, let it be this: paying your bills on time is the single most important thing you can do for your credit health. Payment history accounts for thirty-five percent of your FICO score and up to forty-one percent of your VantageScore. No other factor comes close to wielding this much influence.

Lenders want to know one thing above all else: can they trust you to pay them back? Your payment history provides the answer by creating a detailed record of every bill you have paid on time and every payment you have missed. This category looks at multiple dimensions of your payment behavior. It considers how recently you missed a payment, with recent delinquencies hurting far more than old ones. It evaluates how severe the lateness was, because a ninety-day late payment signals more risk than a payment that was only thirty days late. It also examines the frequency of missed payments across all your accounts.

The impact of a single misstep can be surprisingly severe. For someone with an otherwise excellent credit history, one thirty-day late payment can drop their score by fifty to one hundred points or more. This steep penalty exists because scoring models view a sudden delinquency as a significant change in behavior. The good news is that late payments lose their scoring impact over time, and they must be removed from your credit report entirely after seven years.

Establishing a flawless payment record requires consistency and a few smart habits. Setting up automatic payments for at least the minimum amount due ensures you never miss a deadline accidentally. If you do encounter financial hardship, contacting your lender before the due date can sometimes result in hardship arrangements that prevent the late payment from being reported to the credit bureaus.

Amounts Owed and Credit Utilization

The second most important factor in your credit score is the amount you owe relative to the credit available to you. This category makes up thirty percent of your FICO score and is known in the industry as your credit utilization ratio. While VantageScore breaks this into slightly different components, the principle remains consistent across both models.

Credit utilization measures how much of your available revolving credit you are using at any given time. If you have a credit card with a ten thousand dollar limit and you carry a balance of three thousand dollars, your utilization on that card is thirty percent. The calculation applies both to individual accounts and to your total credit across all revolving accounts. Lenders prefer to see utilization below thirty percent, though consumers with the very highest scores typically keep their utilization in the single digits.

What makes utilization particularly powerful is its responsiveness to your actions. Unlike payment history, which requires months or years to build, utilization can change literally overnight. When you pay down a balance and your credit card issuer reports the new lower balance to the bureaus, your score can reflect that improvement within days. This makes utilization the fastest lever to pull when you need a quick score boost before applying for a major loan.

The relationship between utilization and scoring involves more than just the percentage you use. Scoring models also consider how many of your accounts carry balances. Having small balances spread across multiple cards can sometimes hurt more than having the same total balance concentrated on a single card. The ideal scenario is to use credit regularly but pay it down before the statement closing date, ensuring that the balance reported to the bureaus remains low.

Length of Credit History: The Patience Factor

Time is your ally when it comes to credit scoring. The length of your credit history accounts for fifteen percent of your FICO score and a similar portion of VantageScore models. This factor considers three specific elements: the age of your oldest account, the age of your newest account, and the average age of all your accounts combined.

Lenders prefer borrowers who have demonstrated responsible credit management over many years. A long history provides more data points for predicting future behavior, making you a more predictable and therefore less risky borrower. According to FICO, consumers with the highest credit scores opened their first account an average of twenty-five years ago and maintain an average account age of eleven years.

This does not mean that younger borrowers cannot achieve good scores. A strong payment history and low utilization can compensate for a shorter credit history. However, it does mean that patience is required and that certain actions can inadvertently shorten your perceived history. Closing old credit cards, for example, can reduce your average account age and potentially lower your score. Even if you no longer use an old card, keeping it open allows it to continue contributing to your history length.

The age factor also explains why becoming an authorized user on someone else’s old credit card can boost your score. When you are added as an authorized user, that account’s history may appear on your credit report, instantly increasing your average account age. This strategy must be used carefully and only with someone who manages credit responsibly.

Credit Mix: Demonstrating Versatility

The types of credit you use make up ten percent of your FICO score and are included in VantageScore’s depth of credit category. This factor rewards borrowers who have experience managing different kinds of debt. The two main categories are revolving credit, which includes credit cards and lines of credit, and installment credit, which includes mortgages, auto loans, and student loans.

Having both types of credit on your report demonstrates that you can handle multiple payment obligations simultaneously and manage different account structures. Someone who has only ever used credit cards represents a different risk profile than someone who has successfully managed both credit cards and a car loan over several years.

The key insight about credit mix is that you should never take on debt solely to improve this factor. Opening accounts you do not need creates unnecessary risk and can backfire if you miss payments or carry high balances. Your credit mix will naturally diversify over time as your life circumstances change and you encounter legitimate needs for different types of financing. A young person just starting out may only have credit cards, but eventually they may need an auto loan and later a mortgage. That natural progression builds credit mix without forcing unnecessary borrowing.

New Credit and Inquiries

The final factor in your credit score relates to how recently you have sought new credit. This category accounts for ten percent of your FICO score and is evaluated through both hard inquiries and newly opened accounts. Each time you apply for credit, the lender performs a hard inquiry on your credit report, which typically lowers your score by three to seven points.

Hard inquiries remain on your credit report for two years but only affect your score for the first twelve months. Their impact is generally small and temporary, but multiple inquiries in a short period can add up and signal financial distress to lenders. People with six or more hard inquiries on their credit report are statistically up to eight times more likely to file for bankruptcy than those with none.

There is an important exception to how inquiries are counted. When you are shopping for the best rate on a mortgage, auto loan, or student loan, multiple inquiries within a concentrated window are treated as a single inquiry for scoring purposes. For FICO scores, this window ranges from fourteen to forty-five days depending on the scoring model version. VantageScore uses a fourteen-day rolling window. This rate shopping protection allows you to compare offers without worrying that each application will ding your score.

Opening several new accounts in a short timeframe can also affect your score by lowering your average account age, which ties back to the length of credit history factor. Being strategic about when and why you apply for new credit helps you maintain control over this factor.

Putting It All Together

Understanding the five factors that determine your credit score transforms this mysterious number into a manageable tool. Payment history stands alone as the most important factor, carrying more than one-third of the total weight in FICO scoring models. If you do nothing else for your credit, pay every bill on time, every single month.

Amounts owed and credit utilization follow as the second most critical area, offering the fastest path to improvement when you need to raise your score quickly. Keeping your revolving balances below thirty percent of your available credit, and ideally below ten percent, positions you well for top-tier scores.

The remaining factors, length of history, credit mix, and new credit, play supporting roles that matter at the margins. They reward patience, diversity, and deliberate borrowing behavior. Together, these five factors create a complete picture of your financial responsibility that lenders use to predict your future behavior.

Your credit score is not a mystery or a judgment on your character. It is simply a performance metric based on specific, measurable behaviors. By understanding what goes into the calculation, you can make informed decisions that steadily improve your score and unlock the financial opportunities that come with excellent credit.

Leave a Reply